Crypto Market Report October 2025: macro environment causes cryptos to fall

Published onUpdated on

Sponsored Content

This content was written as part of a commercial collaboration. Although the OAK Research team conducted a preliminary assessment of the project presented, we disclaim any liability for losses or damages resulting from decisions based on this article. Cryptocurrencies involve high risks, and this content is provided for informational purposes only and does not constitute investment advice.

As they do every month, the teams at OAK Research bring you a condensed report on the key information to remember about the crypto market. In this October 2025 edition, we offer a macroeconomic analysis, a market review featuring Bitcoin (BTC), Ethereum (ETH), and the main altcoins, a study of ETFs and Digital Assets Treasury (DAT) companies, and an analysis of the main events.

Macro Environment

Banking sector under stress

October confirmed that the U.S. economy has entered a stagflation regime. Growth is slowing, employment is deteriorating, and inflation remains well above target. For the Fed, the situation is becoming untenable.

Since September, the monetary easing cycle has begun. But this pivot is not necessarily a sign of confidence. It reflects a constraint: a financial system that is short of liquidity.

The Reverse Repo Facility, the Fed’s main liquidity reservoir, is now empty. This safety cushion had been used for three years to defend the U.S. financial system and conduct monetary tightening while limiting the risk of a major crisis.

At the same time, bank reserves have fallen back below 3 trillion dollars, a level considered critical. In addition, the Standing Repo Facility (SRF), designed to offer emergency assistance to banks, has been heavily used in recent weeks, a clear signal of liquidity stress in the interbank market.

Regional banks, for their part, are showing renewed signs of fragility. Zions Bancorporation and Western Alliance both reported sizable losses, echoing the early stages of the 2023 crisis.

The Fed up against the wall

This liquidity stress has a direct impact on monetary policy. As long as the system remains under pressure, the Fed has no choice: it must act to avoid a major banking crisis in the United States. But every rate cut also heightens the inflation risk. This is the dilemma Powell can no longer resolve.

As we noted in our analysis of October 17, the October 29 FOMC confirmed it. The Fed cut rates by 25 basis points while keeping a cautious tone. Officially, it is a simple adjustment. In reality, it is an admission: the system is running out of steam and the Fed has no room left.

Meanwhile, safe havens are surging. Gold has moved above 4,300 dollars per ounce, silver has crossed 54 dollars, and flows into long-dated bonds are rising. These moves reflect a flight to safety, not against inflation, but against the risk of a systemic crisis.

Equity markets remain “artificially” supported by tech and AI, while the real dynamics of the U.S. economy are deteriorating. Unemployment is rising, consumption is slowing, and deficits are widening. At the same time, the dollar is weakening, adding pressure on imports and consumer prices.

In short, the Fed is trapped. If it keeps cutting rates, it reignites inflation. If it stops, it triggers a credit contraction and a liquidity crunch. In both cases, financial stability remains at risk.

October therefore marked a key step: the point at which monetary policy is no longer sufficient to stabilize the system. Stagflation is no longer a hypothesis, the prospects for Quantitative Easing are not yet clear, and this is now the macro backdrop in which markets are operating.

Crypto Market Analysis

Bitcoin (BTC)

October was marked by tension and volatility for crypto markets and for Bitcoin (BTC). After printing a new ATH above 126,000 dollars in the first days of the month, the BTC price ultimately rolled over and ended October down 3.97%.

The first major event was the October 10 crash. In total, more than 20 billion dollars were liquidated in 24 hours, the worst day in the history of the market. Order books emptied within minutes, market makers pulled liquidity, and the drop was catastrophic on many altcoins.

Many traders, even cautious ones, saw positions liquidated with no way out. Despite a swift rebound, the scars are deep: a large portion of retail investors was simply ejected from the market, and the impacts on professional actors remain to be discovered.

→ We published a post-mortem the day after the event. Read it here:

Loading post...

A few days later, on October 17, BTC fell again and stalled for the first time at 107,000 dollars, a key level to preserve the uptrend that started in April 2025. This drop was not trivial, as BTC was entering a zone of uncertainty explained by the macro situation discussed above.

On October 18, we published a full analysis for Premium members. We outlined our view, the key levels to watch, and potential scenarios:

- a sustained recovery above 107,000 dollars to restart the uptrend

- a break below 98,000 dollars to confirm a trend reversal

- and a hold within the range to extend the uncertainty phase

A few days later, the market rebounded exactly as expected. BTC closed above 107,000 dollars on October 20, validating the technical recovery we anticipated. In our October 21 Alpha, we stated that this signal remained valid as long as that zone held on a weekly close, with a short-term target between 112,000 and 115,000 dollars.

That rebound did occur, before price failed below 115,000 dollars at month-end. On a monthly close, Bitcoin fell 3.97% but kept a still-bullish medium-term structure.

However, the first days of November showed a break of the 107,000-dollar level, which in our view is the guardian of this trend. As mentioned in the Alpha Feed, that break pointed to a move back to 98,000 dollars. Looking ahead, that is the level that must hold to avoid a prolonged correction.

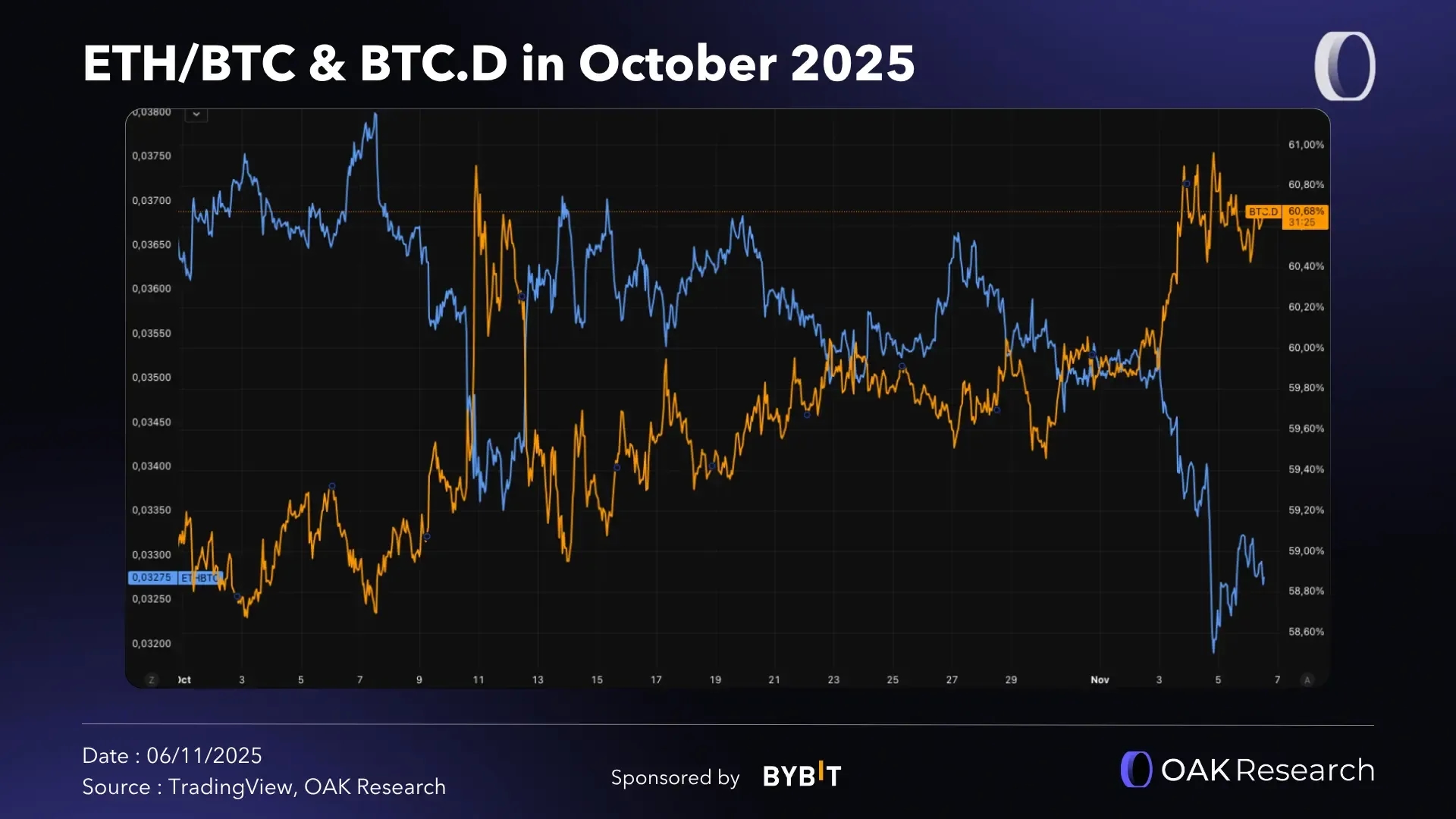

Altcoins and BTC.D

Altcoins did not withstand October’s stress. Ether (ETH) lost 7.2%, from 4,150 to 3,850 dollars. Most other crypto assets followed the same path, often with drawdowns two to three times larger than Bitcoin’s.

BTC dominance (BTC.D) rose 1.45%, back above 59.8%. This increase invalidates the attempted bearish break started in September and confirms that capital flows remain concentrated in Bitcoin. The market is clearly in a “no-risk” phase, where investors still want nothing to do with altcoins.

In previous analyses, we insisted on this point: the altcoin market is not bullish, even when BTC retains positive momentum. That assessment stands. Nothing, at this stage, justifies a “long-term” rotation of flows into secondary assets (aside from a few short-term trades).

Privacy-related tokens were the lone exception. ZCash (ZEC) posted a spectacular gain of more than 445% in the month, while Dash rose 136%. This move remains isolated, but confirms the return of this trend that we already highlighted in our September report.

ByBit Corner

ByBit is the official sponsor of our monthly market report. If you want to open a ByBit EU account (100% regulated in Europe), we invite you to use our partner link.

According to data from Bybit EU, the BTCUSDC pair dominated with 36.26% of trading volumes in October, versus 22.58% and 11.9% in previous months. While SOL and ETH dominated September and August to the point of exceeding BTC in traded volume, that trend fully reversed in October.

Trader behavior logically reflects market conditions. Recent events were a reminder that, for now, only BTC remains in a truly bullish structure and risk is too high for sustained exposure to altcoins.

The return of risk appetite observed in August (19.52% of volumes for ETH, 21.49% for SOL, and even 6.78% for XRP, versus only 11.9% for BTC) faded quickly. Note that the highest-volume day was October 14, 2025.

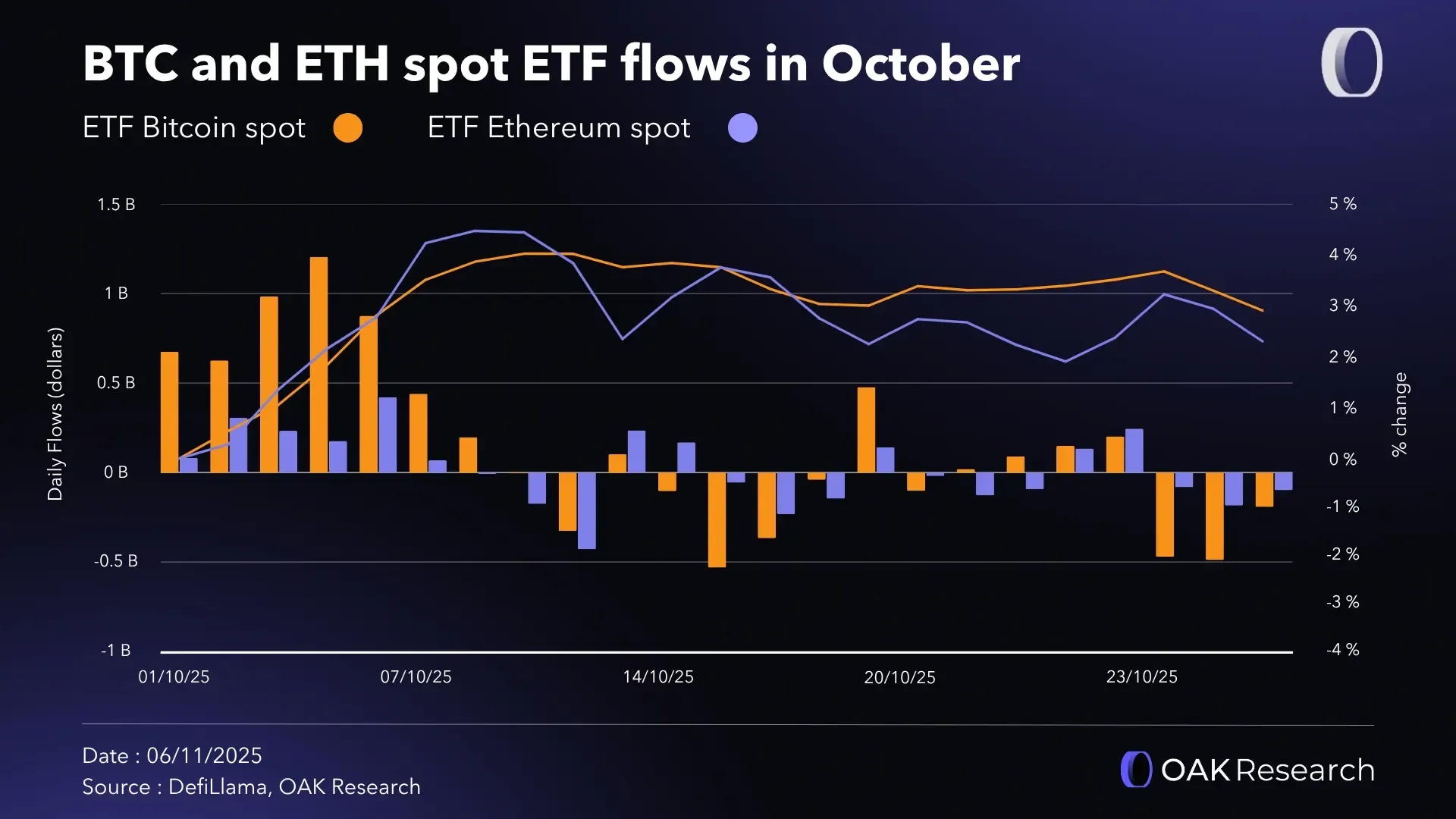

Spot ETFs in the United States

Spot BTC ETFs

Spot Bitcoin ETFs ended October with a positive net balance of +3.42 billion dollars, in line with the previous month. Despite extreme market volatility, flows remained solid, confirming institutional appetite for BTC.

The best day of the month was October 6, with +1.21 billion dollars in net inflows. Conversely, the worst was October 16, with 531 million dollars in outflows, in the wake of liquidity stress and the shock from the October 10 crash.

Compared with September (+3.51 billion dollars), the pace remains steady. This level of inflows signals firm conviction among institutional investors: even in a turbulent month, Bitcoin is still viewed by some as a reserve asset.

That said, these figures need context. The majority of positive inflows occurred during the first few days of October, notably on the ATH day (October 6). By contrast, the market drop over the rest of the month coincided with outflows.

Spot ETH ETFs

Spot Ethereum ETFs posted a positive but more modest balance, with +565 million dollars in net flows for the month. The best day was October 7, with +421 million dollars of inflows, while October 13 saw 429 million dollars in outflows, consistent with ETH’s price decline over the same period.

After a mixed September (+286 million dollars), these flows suggest a gradual return of interest, but without a true fundamental catalyst. Uncertainty around staking and debates over Ethereum’s regulatory status continue to constrain broader adoption.

Despite this caution, the balance remains positive, but again, it is important to note that most inflows occurred during a period of strong euphoria, while the subsequent market drop prompted many to exit positions.

Digital Asset Treasury Companies (DAT)

October confirmed the rise of publicly traded companies that hold crypto directly on their balance sheets. These Digital Asset Treasuries (DAT) have become a structural force in the market, on both Bitcoin and Ethereum, and increasingly on certain altcoins.

As of November 1, 2025, listed companies that hold crypto in treasury are still mostly exposed to BTC with a combined 96.7 billion dollars. This movement is led by Strategy (65 billion dollars) and followed by others (Marathon Digital with 5 billion dollars, Twenty One Capital with 4.4 billion dollars, and Metaplanet with 3.6 billion dollars).

Ether is not far behind, as ETH-focused DAT now hold 17.3 billion dollars. The largest remains BitMine with 11.2 billion dollars. Note that a majority of funds are allocated to staking (direct, liquid staking, or restaking).

In October, the total held by DAT on Ethereum declined (minus 16% versus 20.7 billion dollars on September 30), explained by ETH’s price drop and, to a lesser extent, by some treasury adjustments.

→ Read our Q3 2025 Ethereum report for more details:

Loading post...

Outside BTC and ETH, positions remain concentrated. SOL is still the third dominant asset with about 2 billion dollars held by DAT, notably via Forward Industries (1 billion dollars), Upexi and Sharps Technology (around 300 million dollars each). Exposures to BNB, TRX, XRP, and AVAX remain modest in aggregate.

A new DAT made noise in October: Hyperliquid Strategies. Formed from the merger of Sonnet BioTherapeutics and Rorscharc LLC, the company aims to build a reserve in HYPE with a target above 1 billion dollars. It currently holds 675 million dollars.

The company filed an S-1 with the SEC to raise up to 1 billion dollars through the issuance of 160 million shares, with the explicit intent to buy HYPE and utilize staking. Pending approval, the stock would list on Nasdaq under the ticker PURR. Note that three other companies now complete the HYPE universe: Lion Group Holding (80,000 HYPE), Hyperion DeFi (1.42 million HYPE), and HYLQ Strategy Corp. (54,000 HYPE staked on Kinetiq).

Key News

Polymarket heads to Wall Street

Polymarket is set to raise 2 billion dollars from Intercontinental Exchange, the NYSE’s parent company. The deal includes exclusive distribution of its data by ICE and a joint exploration of real-world asset tokenization. Polymarket is also preparing its return to the United States via the acquisition of QCX (CFTC license) and is studying a token launch, with a raise that could push its valuation toward 15 billion dollars according to the press.

Beyond the financing, the signal is strong for the entire prediction markets segment. Between institutional appetite, gradual regulatory opening, and new products, the “prediction markets war” is truly underway. This opens the door to airdrop strategies and cross-platform arbitrage.

A Solana ETF with staking

Bitwise launched BSOL, the first ETF fully backed by Solana with integrated staking. Creations and redemptions are in-kind, fees are 0% up to 1 billion dollars in AUM (then 0.20%), with estimated staking yield around 7%. A few days after launch, AUM already exceeds 282 million dollars with an average of 50 million dollars in daily inflows.

This product cements Solana as the other major “ETF-compatible” asset after BTC and ETH. It is also a first attempt at staking mechanics within a regulated U.S. product, which could extend to ETH-focused ETFs.

BNB Season, CZ’s return, and new bets

As mentioned in our Alpha Feed, CZ’s return was a strong signal: he is the ecosystem’s biggest KOL and his deep ties to Binance will inevitably push him to promote the BNB ecosystem.

It started with spotlighting Aster, then the launch of “BNB Season.” Driven directly by CZ’s hyper-activity on X, this translated into a wave of performance in BNB Chain memecoins. However, as often in recent months, the market failed to sustain the trend and BNB Season faded within days.

Even so, the presidential pardon granted to CZ strengthens his comeback. Recently, he began promoting OPINION, a prediction market whose volumes briefly surpassed Polymarket on October 25.

Buybacks and the “fee switch”: DeFi professionalizes

Fluid activated the Fluid Reserve, an on-chain reserve funded by revenue to buy back FLUID. First purchase on October 3, and for the first month, 100% of Ethereum revenue is redirected to the reserve, with planned expansion to Plasma, Solana, and the DEX V2. With more than 80% of revenue generated on Ethereum (about 1.7 million dollars per month), the economic engine is clear.

Aave approved a more flexible buyback framework, between 250,000 and 1.75 million dollars per week depending on market conditions, with an annual cap of 50 million. The protocol is also considering a GHO credit line, backed by its treasury, to finance growth strategies.

Ether.fi proposed a new 50 million budget to buy back ETHFI below 3 dollars, but the impact will depend on unlocks, which are still heavy, and on staker reward selling.

Big airdrops ahead

Monad announced its checker this month for one of the most anticipated airdrops in recent months, if not years. More than 225,000 addresses could be eligible, with a window aligned to mainnet launch.

Ink, the L2 backed by Kraken, is pivoting to a stablecoin-oriented chain. The launch of Tydro (lending under Aave licensing) acted as an accelerator, with TVL jumping and explicit hints that activity will count toward the airdrop.

Rabby exposed a “Claim” button in its mobile app, confirming upcoming utility for points accumulated since 2024. Two snapshots have already been taken in 2024, and the DeBank ecosystem could weigh on final allocations. Caution, as always, with fake sites.

MetaMask launched “Rewards,” a points campaign toward an airdrop with seven tiers. Points are distributed for swaps and perps, with bonuses on Linea. The goal is clearly to re-activate wallet usage, though part of the market views it as too extractive.

Finally, Kinetiq announced the creation of its foundation and the launch of the KNTQ token, with 25% reserved for the airdrop and kPoints holders. If you followed our strategies in the Alpha Feed, you should be eligible: sign the terms before November 21 to confirm your allocation.

Note that Meteora’s airdrop disappointed: the TGE ran into a market less receptive to new tokens, in a context where altcoins are struggling heavily, despite an original “Liquidity Distributor” NFT mechanic.

MegaETH: from early raise to public ICO

After a lightning raise on Echo, MegaETH opened an ICO on Sonar. The cap was set at 50 million dollars, for a fully diluted purchase valuation of 999 million dollars. Each participant could bid up to 186,282 dollars.

With more than 50,000 participants and 1.39 billion dollars deposited, MegaETH far exceeded the required amount. Participant eligibility and allocations depend on criteria related to involvement in the ecosystem. The checker will be accessible on Thursday, November 6.