Is USDC actually cooked? Our read on OUSD launch, Circle’s positioning and what changes might occur

Published on

Yesterday $CRCL lost 18% in a single session. Since its ATH in June 2025, three weeks after the company went public, its market cap lost 76% after the initial craze of people looking to gain exposure to the stablecoin narrative. In this article we will present our read on the situation around Open Standard’s OUSD announcement, Circle’s moat, and why we might see some change in how stablecoins operate from now on.

Circle’s Financials: the stock is down, USDC is up

The metric of success for existing stablecoins is the market cap, or in other words, how many digital dollars stablecoin issuers have created. This metric translates demand, usage, and success of a company. Today, most of stablecoin issuers are private companies, meaning that no one can access their actual revenue, or bet on their success by acquiring shares.

When Circle went public in 2025, this changed. Now, Circle’s valuation depends on various factors besides the number of circulating USDC. Investors care about revenue, future potential, and whether Circle will be the one getting the largest share of the stablecoin pie in the long term.

Let’s take a look at the financial situation of the company.

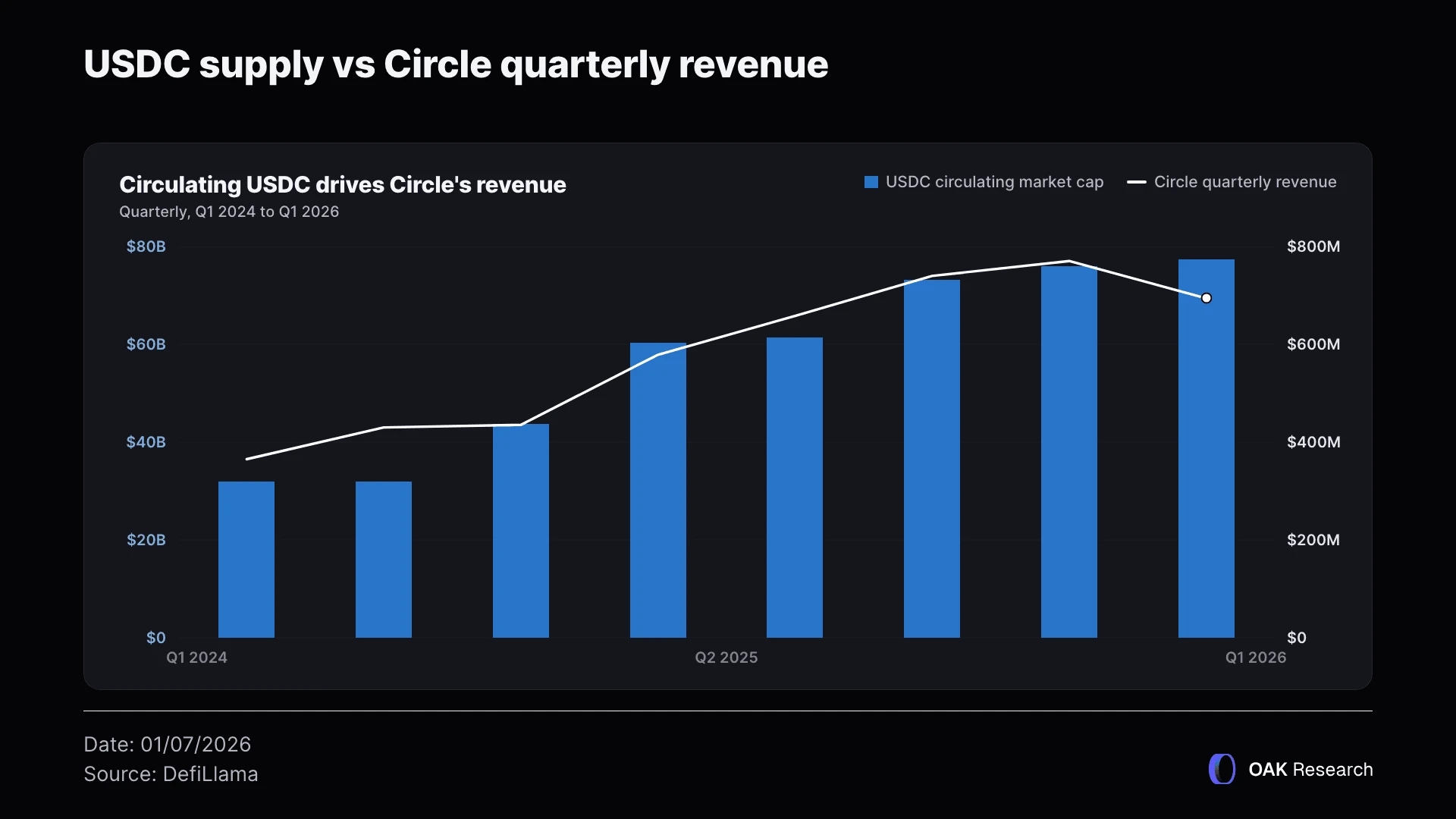

Circle's quarterly revenue climbed from $658.1M in the IPO quarter to $694.1M in the most recent quarter, up 5.5% since the company went public. Over the same window, USDC's circulating market cap grew from $61.3B to $77.4B, up 19.9%, roughly 3.5 times faster than the revenue.

What this means is: Circle is capturing steadily less of that growth as fee income. Net income margin has fallen every quarter since the post-IPO trough: 29.0% in Q3 2025, down to 17.3% in Q4, down to 8.0% in the quarter just reported, and revenue itself posted its first sequential decline, down 9.9%, in that same quarter.

This also means that CRCL’s stock has suffered from the repricing of the company’s future positioning and potential revenues in an ever-increasing competition. Most of the revenue Circle generates (94%, according to Circle’s Q1 10-Q filing) comes from USDC reserves (mostly T-bills), precisely the part Open Standard emphasized will be redistributed to all partners of the network.

The Nail in the Coffin: OpenStandard's Open USD

On June 30th, a new stablecoin was unveiled while Circle’s CEO Jeremy Allaire was on the stage at the Goldman Sachs Digital Assets conference in London talking about “Stablecoins and the Future of Money”.

Open Standard announced its launch later this year with the backing of 149 partners that include both TradFi giants such as Visa, Mastercard, Blackrock, BNY Mellon, Google, IBM, Shopify, or Stripe, as well as Crypto companies such as Aave, Tempo, leading CEXs (Bybit, OKX, Gemini, etc), Plasma, or, the one that hit Circle the hardest, Coinbase.

OUSD is a dollar stablecoin with no minting or redemption fees that distributes nearly all reserve yield back to the partner businesses that adopt and use it.

Notably, neither Tether, Paxos, or Circle were announced as part of the coalition, and coverage from multiple outlets framed the project explicitly as a direct challenge to both incumbents.

This launch was the final nail in the coffin for Circle that has faced several headwinds over the past few weeks:

- Binance is suspending its services in the EU after failing to secure a MiCA licence. Circle paid Binance a one-time $60.25M fee plus ongoing monthly incentive payments tied to Binance holding a minimum $1.5B of USDC, as part of a broader two-year global promotion deal signed in November 2024. This means no USDC for European users on Binance.

- CRCL stock removed from multiple Russell Growth Indexes: Simply Wall St reported that Circle’s stock was removed from several major Russell Growth Indexes during the Russell annual reconstitution on June 26 (Russell 1000 Growth Index, Russell 3000 Growth Index, Russell Midcap Growth Index.) This means that passive funds that invest in these indexes will have to reduce their exposure, affecting liquidity around rebalancing rates.

Become Premium

Unlock all our research and get the right insights, at the right time.

Circle's Remaining Edge

Circle is not dead, but it’s suffering. Its genuine moat remains its proximity to regulators, lobbyists, and its first-mover advantage.

- Circle’s regulatory moat

Circle's regulatory head start is deeper than a general "they're compliant” or “they are close to the regulators”.

Circle holds money transmitter licenses in 46 US states and is known as being THE “American” stablecoin by choice.

In December 2025, Circle received conditional OCC approval for a national trust bank charter making USDC GENIUS Act-compliant.

On July 1, 2024, Circle became the first global stablecoin issuer to achieve full MiCA compliance in the EU, securing an Electronic Money Institution license from France's ACPR before the bloc's stablecoin rules even took effect. Therefore, USDC and EURC are the two stablecoins authorized to be traded in the EU.

This MOAT took Circle years to build, and even with a successful launch, OUSD has some regulatory headwinds ahead that they will have to take care of before challenging Circle’s dominance.

- Hyperliquid and AQAv2 Framework

The Hyperliquid relationship is a more interesting case for how much of that edge Circle actually monetizes. Under Hyperliquid's AQAv2 framework, passed by validator vote in June 2026, Circle and Coinbase (as USDC's technical and treasury deployers on the chain) must share roughly 90% of the reserve yield earned on Hyperliquid-held USDC with Hyperliquid's own Assistance Fund, which uses it entirely for HYPE token buybacks.

Since this vote passed, USDC has become the main stablecoin used on Hyperliquid, while Native Markets sunset its USDH, a Hyperliquid-aligned stablecoin that won the bidding in September 2025.

Hyperliquid has become the main venue for perp trading with a supportive community and a token that outperforms most cryptocurrencies thanks to the HYPE buyback program.

It is, however, worth noting that while the Hyperliquid integration has a good look for Circle, roughly $5 billion reserves generate little to no revenue for the company as 90% of the revenue the reserves generate flows towards HYPE buybacks.

- Integrations, liquidity, and first-mover advantage

Circle was launched in 2018 and has a long history of compliance, audits, and regulatory support behind it.

Circle's Payments Network already counts Santander, Deutsche Bank, Société Générale, and Standard Chartered as original design partners, alongside others. USDC is the main collateral for trading on most CEXs in the EU and the US. USDC has been the settlement asset for BlackRock's BUIDL tokenized fund since April 2024. BNY Mellon (one of OUSD’s launch partners) made USDC the first stablecoin on its Digital Asset Custody platform on June 29th 2026, letting institutional clients mint and redeem USDC directly through an account they already trust.

Put together, these three angles describe a moat that is real but is becoming narrower. Circle is still the counterparty institutions default to when they want a regulated dollar with nearly a decade of audit history behind it. As stablecoins progress and competition toughens, Circle will have to make significant changes to its business to keep its customers without losing them to new initiatives like OUSD.

Tether feels unbothered by this launch

While most of CT was trying to figure out the impact this launch would have on Circle and Paxos, Tether’s CEO Paolo Ardoino put out a simple tweet taking his chance to take a shot at Circle.

Loading tweet...

At the same time, Tether’s dominance has been stable over years. While maintaining a slower growth rate (16.5% over the last 365 days over Circle’s 19.9%), USDT is the market leader with over 180 billion USDT in circulation today.

Where Tether's moat really shows up is distribution geography. USDT's supply is concentrated on Tron (47.6%) and Ethereum (42.8%), together more than 90% of its float. Tron's role is well-documented as a low-cost settlement rail for remittances and peer-to-peer transfers in emerging markets rather than DeFi. Tether has also been actively investing in that sector, including a strategic stake in remittance platform LemFi aimed at embedding USDT into Africa and Asia payment flows.

At the same time, USDT is also the most important collateral for trading across CEXs outside of Europe, especially in Asia. Our read here is: Tether is less concerned by this launch than Circle as it remains the settlement layer in the regions OUSD will not necessarily target. However, Tether is not a public company, therefore the external perception is not visible in the company’s stock valuation.

Subscribe to Blocknote

Your weekly crypto digest delivered directly to your inbox.

OpenStandard's Hurdles

Now that we’ve covered the Circle situation and Open Standard’s launch impact on its business, it is worth talking about OUSD and the potential hurdles the company might have once its stablecoin launches.

- New stablecoins tend to disappoint

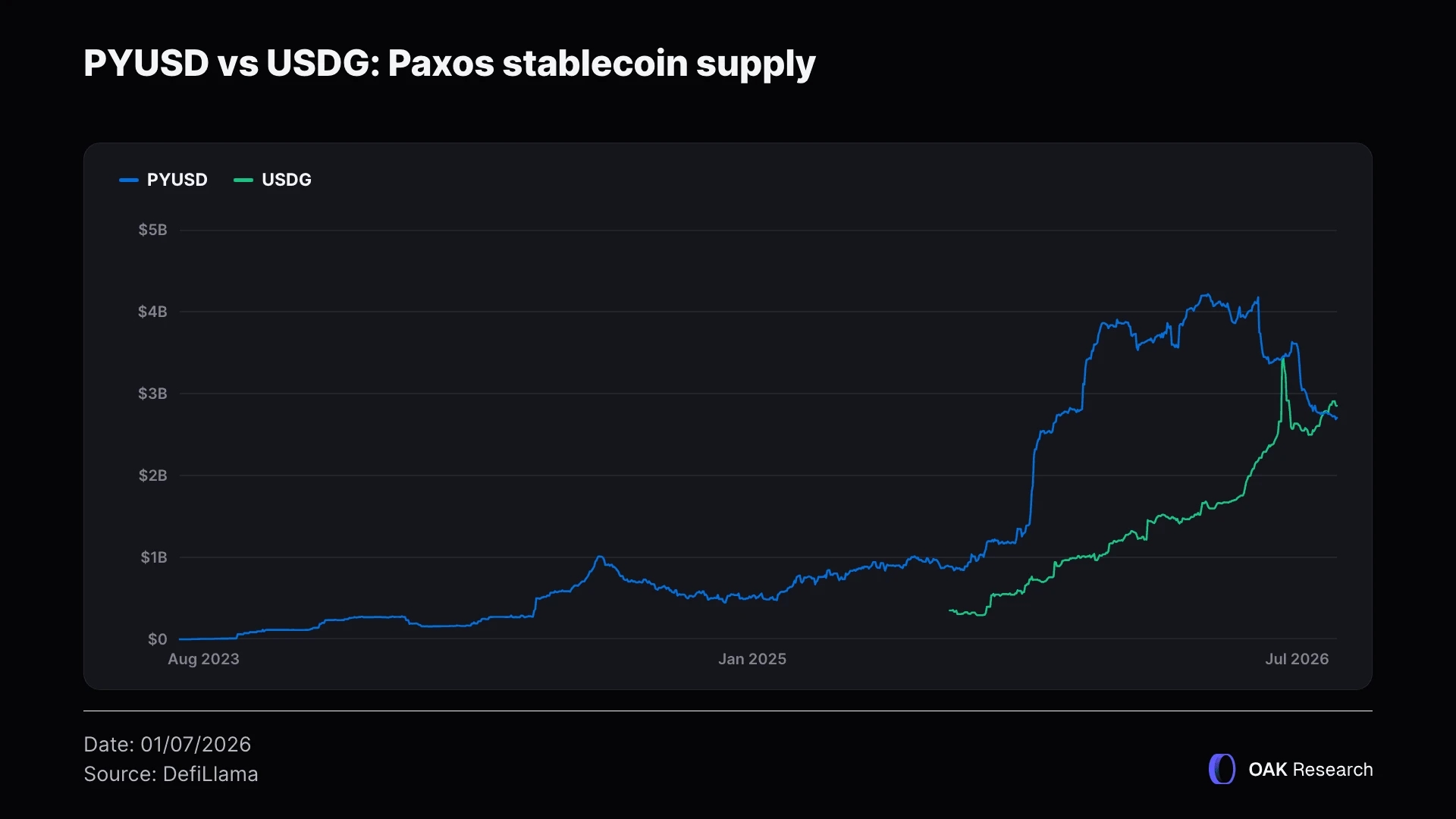

The precedent case is not encouraging for fast adoption. Paxos's USDG, backed by a similar consortium model including Kraken, Robinhood, Galaxy Digital, and Anchorage, took roughly 4 months to reach $1B in supply and is currently sitting at around $3B, still well under 4% of USDT's size.

PayPal's PYUSD case is even worse: it took 383 days to reach $1B and 921 days, roughly 2.5 years, to peak near $4.2B, and has since contracted to $2.69B, a decline of around a third from its peak. Both examples support the same conclusion: unless you are able to align incentives and attract liquidity, your stablecoin will remain a marginal use case for most users.

- Consortiums are hard to manage

Open Standard’s announcement produced a bang because of the 149 big names from TradFi and Crypto. The announcement reads

“Open USD will be operated by Open Standard, an independent company with a board made up of Open USD’s partners, ensuring decisions are made for the collective interest, not a single entity.”

As we have seen in DAOs, and other organizations with multiple members, coordination is the most important part: it allows you to move fast, take meaningful decision quicker, and integrate with new partners more efficiently without asking for the permission of the board.

“Large groups of large companies coordinate poorly, have misaligned incentives, slow things down and rarely create the space for real durable innovation and competitiveness. They also typically, out of their own self-interest, starve the consortium itself on an operating basis.” - Jeremy Allaire, CEO of Circle on X

We do have to agree with this statement even though it is coming from someone whose stock tumbled 18% after the announcement.

- Open Standard’s revenue

Just like with Circle and Tether, most of the revenue comes either from mint and burn fees, or from interest generated on the reserves. In OUSD’s case, both streams of revenues are absent from the business model outlined in the announcement.

“Businesses can mint and redeem Open USD at no cost and with no artificial limits on volume.”

“Partners receive all of the earnings from Open USD’s reserves, less a small management fee to cover Open USD’s operational costs.”

The question raised is the profitability of this venture and whether its aim is actually making money.

It is also interesting that the interest generated by OUSD’s reserves will flow back to its partners, not the users. This means that banks, chains, and infrastructure providers will be the ones receiving the yield. This does not really encourage the end user to hold this stablecoin. It remains to be seen if the launch partners will redistribute the yield back to their users.

- Incentives and deployment

Every new stablecoin issuer has to independently bootstrap market makers and liquidity pools rather than inheriting the existing ones. OUSD will face the same problem, compounded by the fact that, as of its announcement, Open Standard had not yet named which blockchains it will launch on, but looking at its partners you might get an idea.

In the initial announcement, 8 chains are named as partners of the launch. These are: Solana, Base, Stellar, Polygon, Aptos, XRP (Ripple), and most importantly two stablecoin-focused chains Plasma and Tempo.

We believe that these two last chains are the ones to watch for the launch of OUSD.

Tempo is the chain launched by Stripe. Stripe acquired Bridge. Bridge’s co-founder and CEO is also the CEO of Open Standard. Stripe can simply distribute incentives that will propel its own chain to new TVL highs by distributing stablecoins to those using the chain.

For Plasma, we believe there are two things at play. The first one is its neobank, Plasma One. Plasma’s goal is to make people spend cash with their card, while growing its chain TVL. We believe that incentives might come from both Plasma team and Open Standard’s team as they are clearly targeting payments.

Aave is also one of the launch partners. The protocol has the biggest TVL on Plasma, right after Ethereum and already integrates USDe often used for looping and leverage. We believe that some opportunities may arise there too and will cover these once the launch date is confirmed on our X account.

Circle has dug its own grave, but might still recover

When Solana's Drift Protocol was exploited for $295M on April 1 2026 , roughly $230M in stolen USDC was bridged from Solana to Ethereum through Circle's own CCTP infrastructure across more than 100 transactions over a six-to-eight hour window during US business hours, with no intervention from Circle. ZachXBT flagged the transfers in real time, but Circle never took time to freeze these assets.

Days later, Zach published a broader thread alleging $420M+ in cumulative compliance failures across 15 documented cases since 2022.

Loading tweet...

Tether CEO Paolo Ardoino publicly accused Circle of running a "kill Tether" campaign disguised as compliance advocacy, saying competitors' real business model shifted from building better products to lobbying for monopoly.

Circle publicly embraced the GENIUS Act's ban on stablecoin issuers paying yield, framing it as a "structural feature" that draws a clean line between payment rails and investment products. This directly affects the end user experience, while giving a clear advantage to Circle’s partners such as Coinbase that are able to circumvent this rule by drawing agreements of payment for distribution rather than distributing the yield.

Circle's core business did not collapse this week, but the market reaction showed that its moat could be weakened. For years, a lot of actors in crypto publicly called out Circle for being “suits-aligned”, while dismissing its core flaws.

With OUSD’s launch, however, the cracks have started to show: Circle is not the only player in the stablecoin field anymore, its margins will likely continue to compress as Circle shares more revenue with its partners, and its regulatory moat will continue to be a less important argument once regulators set the bar for everyone.

Start Trading on Hyperliquid

Trade 100+ perps with up to 40x leverage on a fully decentralized exchange.

One thing is clear: if one of the main players of the industry rushes to purchase a Wall Street ad after your announcement, that its CEO has to issue public statements that address questions asked by their shareholders, and that most of the employees of the company constantly retweet bearish takes on the OUSD launch made by people heavily invested in the same competitor in panic mode, you know you are doing something right.

The success for OpenUSD remains to be seen and there are a lot of hurdles to overcome. On our end, we welcome the competition that will benefit the end users and provide more choice in the stablecoin landscape.