Crypto market report November 2025: The Discipline of Holding

Published on

Sponsored Content

This content was written as part of a commercial collaboration. Although the OAK Research team conducted a preliminary assessment of the project presented, we disclaim any liability for losses or damages resulting from decisions based on this article. Cryptocurrencies involve high risks, and this content is provided for informational purposes only and does not constitute investment advice.

As every month, OAK Research brings you a concise report covering the key developments in the crypto market. In this November 2025 edition, we provide a macroeconomic overview, a market analysis featuring Bitcoin (BTC), Ethereum (ETH) and major altcoins, an examination of ETF and Digital Asset Treasury (DAT) trends, and a review of the main events that shaped the ecosystem.

Macroeconomic Context

November 2025 extended the period of tension we have been describing for several months. The US financial system remains fragile, the Fed has little room to maneuver, and markets now operate in an environment that can be summed up in one word: uncertainty.

The impact of the US government shutdown

The end of the 43-day US government shutdown did not ease concerns. On the contrary, it created a true statistical blackout: inflation and employment figures for October were never released, even though they are the most important macroeconomic indicators.

The Fed has historically operated with a data-oriented approach, meaning decisions are based strictly on observable economic data. This blackout therefore has two consequences. Jerome Powell is forced to navigate without visibility, and investors lose the benchmarks they usually rely on to anticipate policy decisions.

This lack of information amplified uncertainty across markets, pushing many investors toward more liquid positions and accelerating the de-risking trend already underway throughout the month.

At the same time, internal stresses within the US financial system remain unresolved. The Reverse Repo Facility is still empty, banking reserves continue to sit below critical thresholds, and the NFIB index confirms the deterioration of the real economy. In other words, structural stress is not improving.

Japan pressures global markets

Another key factor in November came from Japan. Over the past weeks, Japanese government bond yields have risen sharply. The 10-year yield now exceeds 1.9 percent, the 20-year approaches 3 percent, and markets increasingly expect a Bank of Japan rate hike in December.

This shift challenges one of the pillars of global finance: the yen carry trade. For nearly three decades, investors have borrowed in yen at near-zero rates to deploy capital abroad, notably into US Treasuries.

If Japanese yields rise and become genuinely attractive, the incentive for this strategy disappears and investors are encouraged to repatriate capital back to Japan. In other words, a major source of global liquidity could contract precisely when the Fed is already trying to avoid a bond market crisis.

This adds further pressure on the United States. Lower demand for Treasuries would raise long-term yields and shrink the Fed’s ability to ease monetary policy. In an already fragile environment, this external pressure represents an additional risk that markets had anticipated but is nonetheless negative.

The end of Quantitative Tightening

The only positive signal of the month came from the Fed, which officially announced the end of Quantitative Tightening effective December 1st. After several years of aggressive balance-sheet reduction, the central bank now acknowledges that the US financial system cannot sustain further liquidity withdrawal.

However, this move is far from enough to reassure markets. Powell stated clearly that a rate cut in December is not guaranteed and provided no timeline for any future Quantitative Easing program.

More importantly, the Fed is not just ending QT. It is adjusting the composition of its balance sheet. Currently weighted toward long-dated securities, the balance sheet will be gradually shifted toward shorter maturities. Most analysts interpret this as a form of indirect QE.

This technical adjustment allows the Treasury to continue issuing short-term debt while the Fed absorbs the supply without formally restarting asset purchases. Market liquidity is not immediately constrained, but Powell avoids sending too strong a signal too early. This hybrid strategy offers mild relief while delaying an explicit easing cycle.

In summary, despite the end of QT, the Fed still lacks room to maneuver and markets continue to operate in an environment dominated by limited visibility. With no reliable macro data and mounting external pressure, investors have little to guide their expectations ahead of the December 11 FOMC meeting. This explains the persistent volatility throughout the month.

Crypto Market Analysis

November was marked by a sharp correction across the crypto market, driven by significant macroeconomic uncertainty. As we anticipated for several weeks, the combination of an exhausted US monetary cycle and a statistical blackout induced by the shutdown triggered broad de-risking.

Bitcoin (BTC)

BTC fell by 17.3 percent in November, moving from 109,400 dollars to around 90,400 dollars, with an intraday low near 80,400 dollars. This move unfolded exactly in line with the scenarios we described in October.

The loss of the 107,000 dollar level, identified as the key support sustaining the uptrend since April, was confirmed early in the month. In our previous Premium analyses, we explained that a daily close below this level opened a logical move toward 98,000 dollars.

This second threshold, described as the final support for the uptrend, also failed. The breakdown triggered a wave of liquidations and systematic repositioning from quant models, pushing BTC into the 85,000 to 88,000 dollar zone, exactly the area we had identified as an intermediate support.

The 75,000 dollar level, considered the next target in case of deeper deterioration, has not been reached yet.

Beyond the technical structure, our thesis remains the same. BTC’s trajectory now depends almost entirely on expectations of significant monetary easing from the Fed. Without that catalyst, the market struggles to establish a sustainable bullish structure.

The statistical blackout reduced the market’s ability to estimate the future path of rates, and this uncertainty was immediately reflected in BTC’s price. Even with QT ending and the probability of a December rate cut exceeding 90 percent, the market has not yet found the conditions for a constructive rebound.

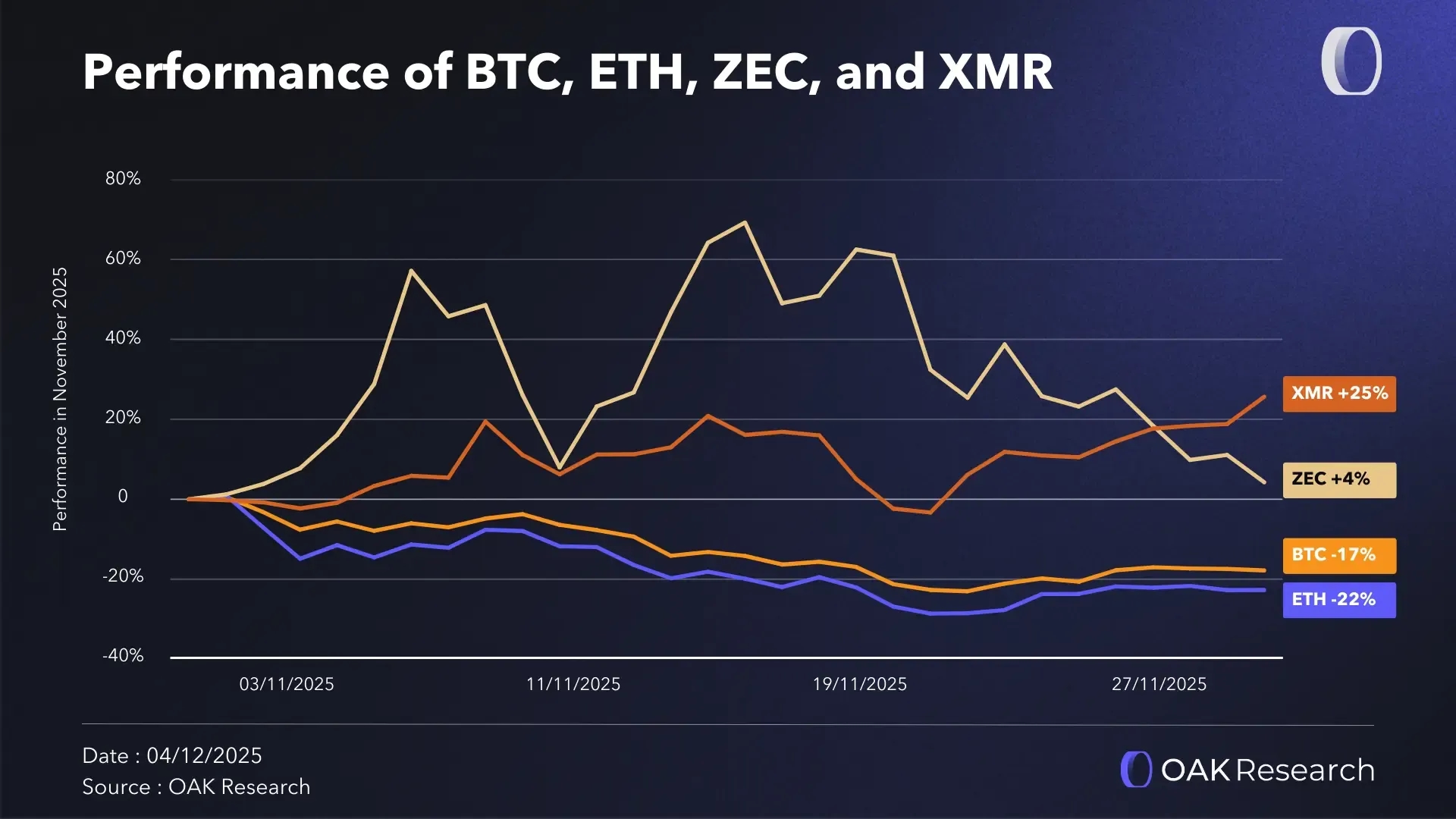

Ether (ETH), altcoins and dominance

ETH underperformed BTC in November, falling by 21.9 percent from 3,800 dollars to below 3,200 dollars, with lows sub-2,600 dollars. This decline extends a multi-month trend in which ETH and most altcoins have struggled to find an independent catalyst in a macro-driven environment.

One notable point, however, is ETH’s relative resilience at the end of the month, which helped limit the rise in BTC dominance. This strength was supported by significant deleveraging across altcoins since October and defensive rotation toward the least risky assets.

BTC dominance ended the month almost unchanged, rising only 0.79 percent. Historically, sharp BTC corrections lead to even sharper declines in altcoins, which typically push dominance higher. The absence of such a move is unusual.

Despite the negative backdrop, certain sectors outperformed. Privacy-related assets showed strong gains, while the AI sector recorded one of the sharpest corrections near minus 25 percent.

In general, the behavior of BTC dominance reflects the extent of prior altcoin deleveraging and ETH’s relative recovery at the end of the month. Our stance remains unchanged. In a macro environment dominated by uncertainty, there is no compelling reason to hold altcoin exposure.

Bybit Corner

Activity on Bybit EU increased sharply in November. November 17 was the most active day of the month, with volumes twice as high as the peak observed in October. The data confirms a stronger concentration on major assets in a context of elevated volatility.

BTC now accounts for nearly 30 percent of all trades and roughly one third of total volumes, compared to 13 to 17 percent in October. Users clearly shifted back toward BTC at the expense of altcoins, a typical pattern during corrective phases. ETH volumes remained stable and broadly aligned with the rest of the market.

Small-cap assets such as XRP, DOGE and LINK saw a visible reduction in activity, while speculative pairs fell sharply. PEPE declined to 4.32 percent of volumes in November from 10.68 percent in October.

Stablecoin and EUR pairs held steady around 10 percent, indicating solid deposit flows and consistent arbitrage activity between fiat and stablecoins. This suggests that European inflows remained resilient despite market uncertainty.

We also highlight the end-of-year 2025 campaign launched in partnership with Bybit EU for OAK Research subscribers. This offer comes in addition to the existing French campaign and provides an extra 30 USDC when opening an account, on top of the current bonuses:

- 25 USDC for a deposit of 100 euros

- 25 USDC for placing 100 euros in Earn for 7 days

In total, new users can receive up to 80 USDC when creating an account on Bybit EU. To access the offer, please use our official link.

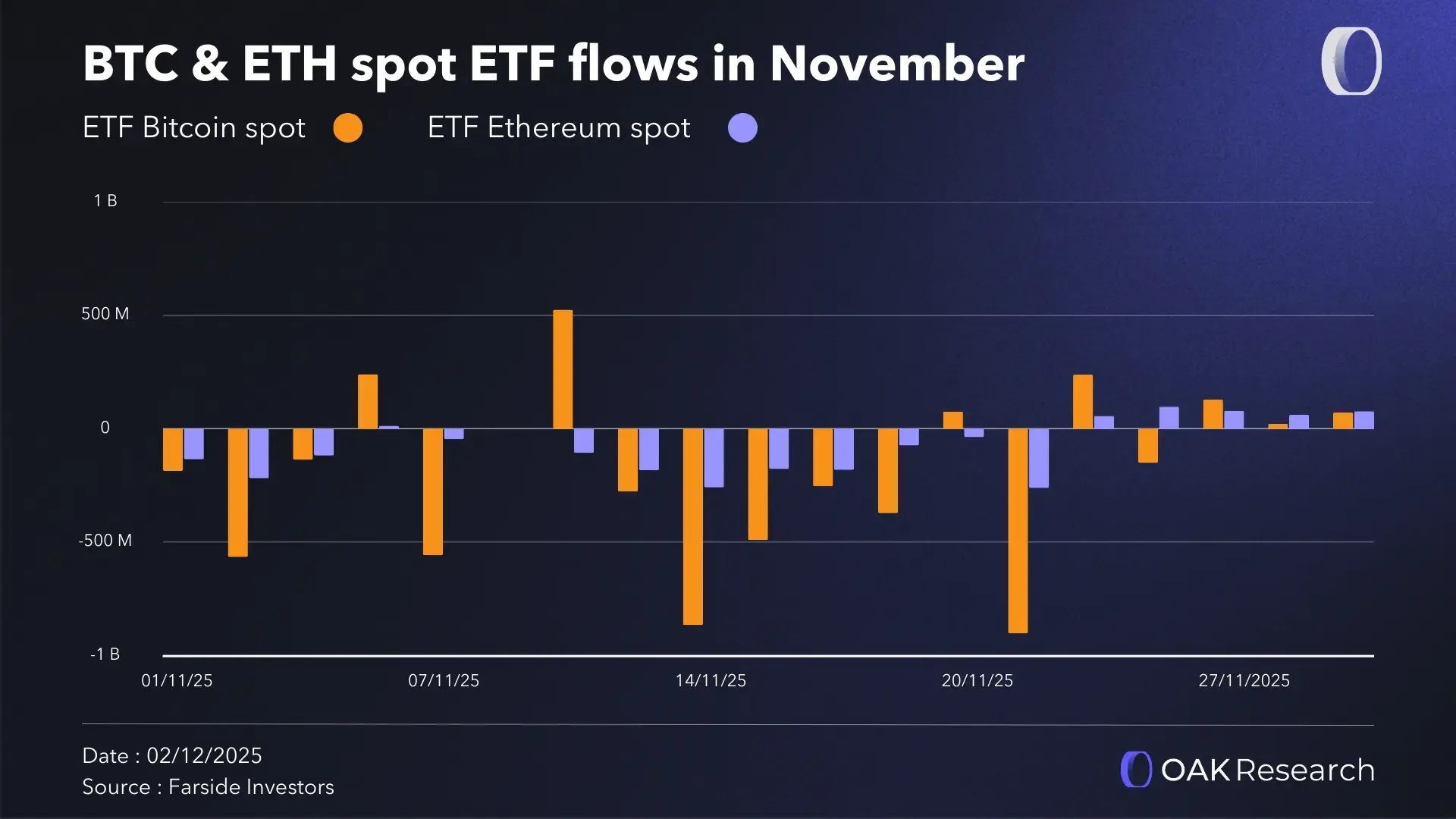

Bitcoin and Ethereum Spot ETFs

Bitcoin spot ETFs recorded their first clearly negative month since spring, with approximately 3.5 billion dollars in net outflows during November. Most of these outflows occurred during the first half of the month, when expectations for rapid Fed easing were most contested.

The largest contribution came from BlackRock’s IBIT, which saw roughly 2.34 billion dollars in net outflows. Twelve sessions ended in negative flows, compared with only five positive sessions, including a five-day streak of red days starting on November 12.

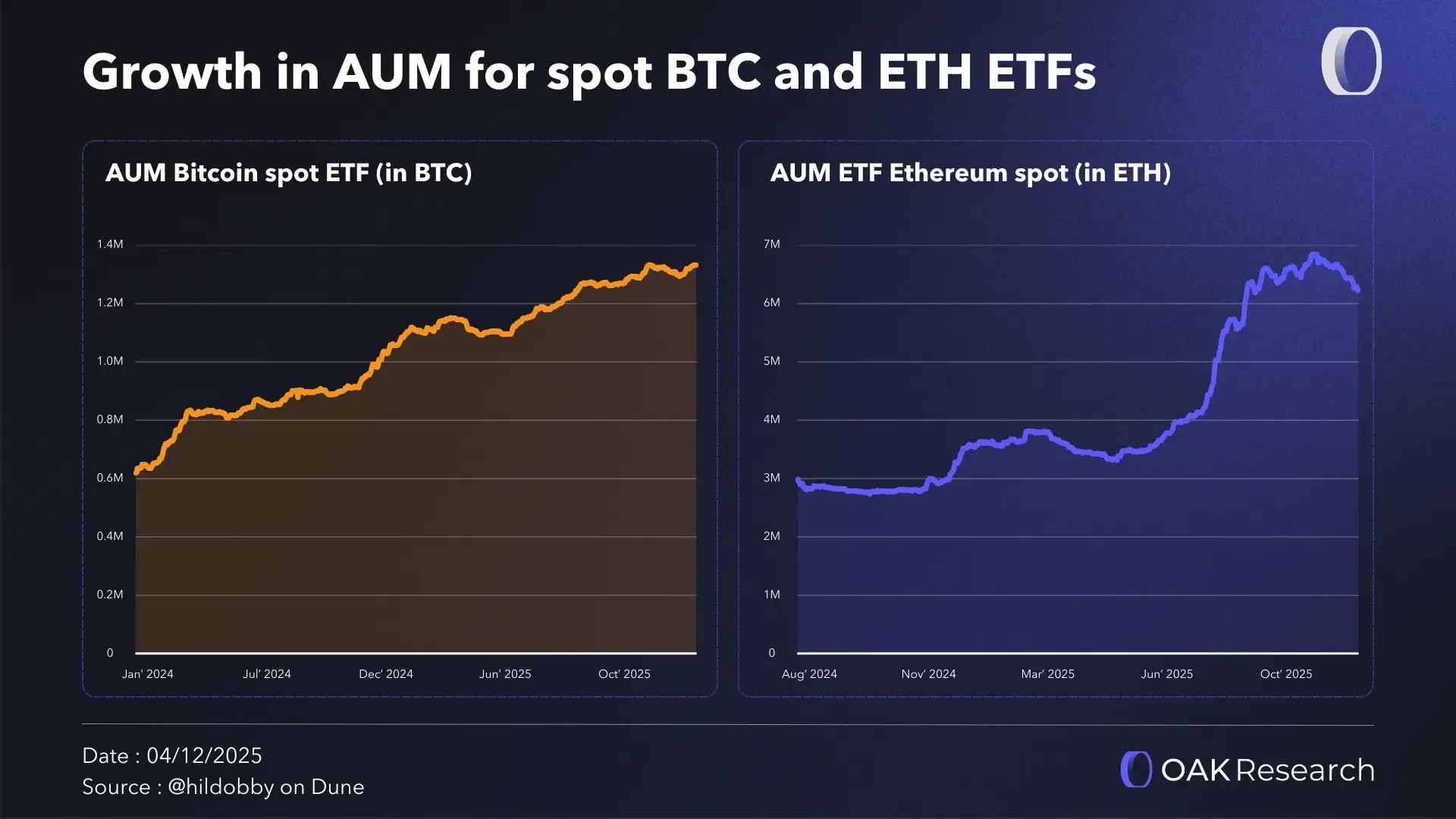

Despite these outflows, BTC holdings in spot ETFs remained broadly stable. ETF balances stood near 1.32 million BTC at the start of November, dipped toward 1.29 million at the monthly low, then recovered slightly above 1.32 million by month end. The decline in AUM in dollar terms was driven primarily by BTC’s price drop rather than a collapse in holdings.

Ethereum spot ETFs were similarly impacted, with 1.42 billion dollars in net outflows. Total holdings fell from about 6.61 million to 6.23 million ETH, a decline of roughly 5.8 percent in underlying assets. Dollar AUM fell to around 18.8 billion dollars, the lowest since July and more than 40 percent below the peak recorded in early October.

The largest outflows were concentrated in BlackRock’s ETHA, including several sessions with steep withdrawals and a mid-November peak near 180 million dollars in a single day.

At the same time, newly launched spot ETFs saw positive inflows. XRP ETFs attracted around 660 million dollars, Solana ETFs 531 million dollars, and other thematic or Web3 ETFs around 280 million dollars.

Major November Developments

Stream Finance and the collapse of xUSD

November saw the collapse of Stream Finance, whose stablecoin xUSD progressively depegged until it traded near 0.04 dollars. Behind the collapse was an aggressive minting loop operated by the team using client funds.

User deposits in USDC were routed through multiple internal addresses, converted to USDT, used to mint deUSD, staked, rehypothecated as collateral on Elixir, borrowed against, reconverted, bridged and re-used in repeated loops.

Stream also minted its own xUSD stablecoin, used as collateral to borrow USDC on Morpho, with Elixir supplying liquidity that itself originated from the same loop. In other words, both sides were lending to each other to inflate TVL while exposing user funds to extreme risk.

The situation worsened after the Balancer hack triggered widespread withdrawals across DeFi. xUSD began losing its peg, and shortly after, Stream disclosed that an external manager had lost 93 million dollars. Deposits and withdrawals were frozen.

The depeg spread to integrated protocols using hardcoded xUSD prices, preventing liquidations and amplifying systemic losses. Estimates suggest roughly 285 million dollars of bad debt. Stream Finance has now shut down.

Uniswap activates the fee switch and recenters around Labs

A major governance proposal was introduced on Uniswap, the long-awaited Unification Proposal. Its goal is to activate a true fee switch by redirecting part of trading fees on Uniswap v2 and v3 toward an automated buyback and burn mechanism for the UNI token.

The plan allocates 0.05 percent of the 0.30 percent fee on v2, and a share of LP fees on v3, directly into the burn mechanism. Additional revenue sources would also be included, such as Unichain sequencer fees and the Aggregator Hooks introduced with Uniswap v4. The proposal also includes a retroactive burn of 100 million UNI from the DAO treasury.

In parallel, Uniswap proposes a major restructuring of its governance by transferring the functions of the Foundation to Uniswap Labs. This change transitions Uniswap toward a more centralized operational model while retaining decentralized components at the protocol level.

Although criticized for reducing decentralization, the move reflects a reality of the market. Investors are increasingly focused on holding assets tied to real cash flows rather than participating in governance. Major protocols across the ecosystem have gradually moved toward hybrid governance structures, and Uniswap now aligns with this trend.

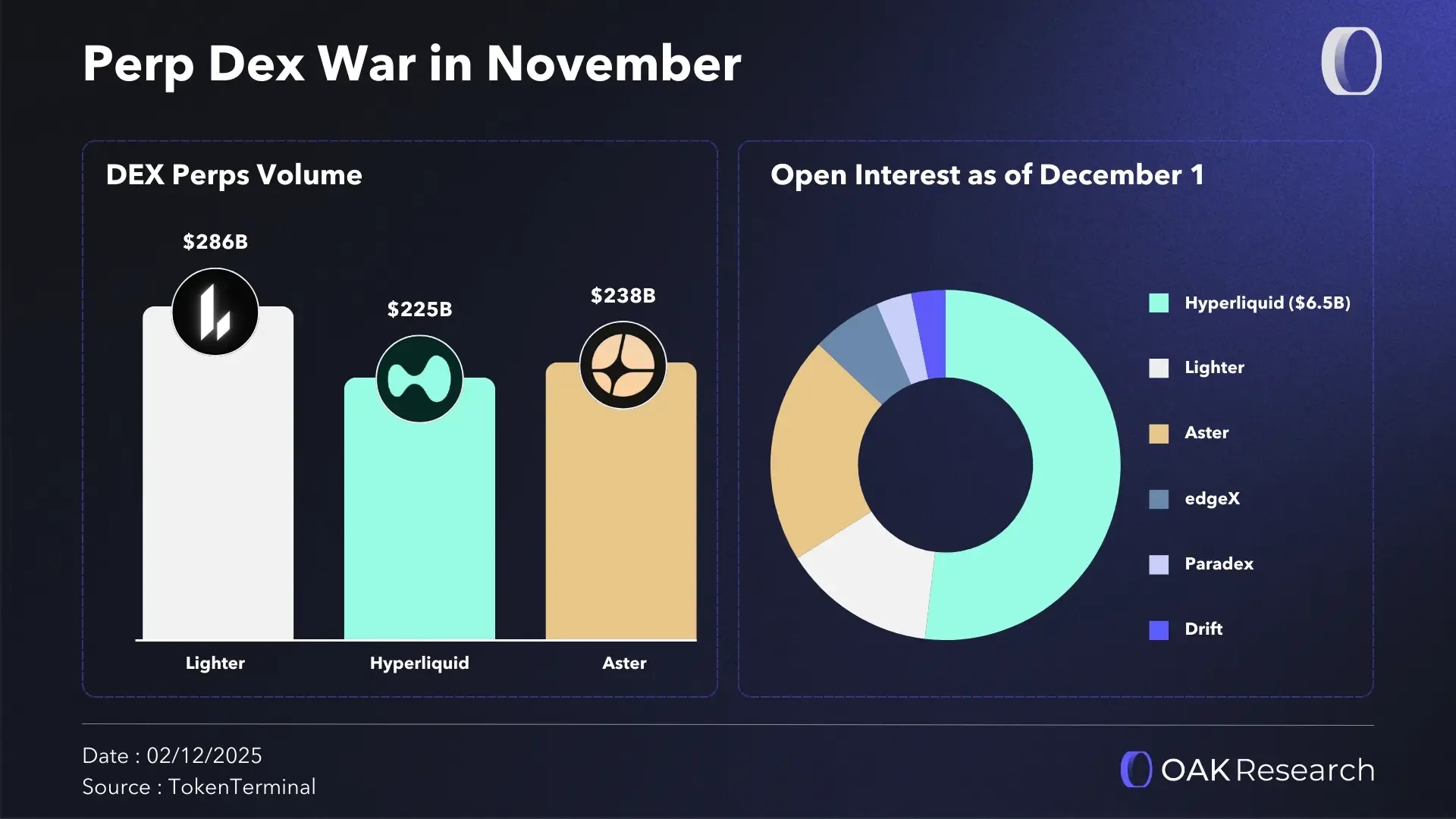

Lighter raises 68 million dollars and strengthens the perp DEX narrative

Lighter, one of the leading perpetual DEXs, announced a 68 million dollar raise valuing the project at 1.5 billion dollars. Participants included Founders Fund, Ribbit Capital, Haun Ventures and Robinhood. Tokens will be allocated at TGE.

This raise marks a clear break from the no-VC positioning that contributed to Hyperliquid’s success, but it sends a strong signal. Perp DEXs are no longer seen as a speculative niche but as a durable market vertical capable of attracting institutional capital and justifying DeFi blue chip-level valuations.

In November, Lighter became the top perp DEX by trading volume with 286 billion dollars, setting a new record. Despite zero fees for users, the protocol captured 25 million dollars of revenue from market makers. Hyperliquid recorded 225 billion dollars in volume, its lowest since June, placing it behind Aster, though it still dominates in open interest.

→ Find our guide to farming DEX perps airdrops and our regular updates in the Alpha Feed:

Loading post...

Aerodrome and Velodrome merge to form Aero

Dromos Labs officially announced the merger of Velodrome and Aerodrome into a single protocol named Aero. The new protocol will become multichain, launching on Base, Optimism, Ethereum and Arc in 2026.

Migration to the unified AERO token will be allocated according to historical revenue contribution from each protocol. This consolidation aims to strengthen liquidity, emissions and governance under a single coherent structure, reinforcing the ve(3,3) flywheel.

By aligning branding, tokenomics and revenue flows, Aero provides a clearer value proposition to users, LPs and partners, while preparing the ecosystem for future expansion.

Aave confirms its pivot toward on-chain neobanking

Aave confirmed its strategic move toward the retail market. After acquiring Stable Finance, a US fintech offering mobile stablecoin savings, Aave launched Push, a regulated subsidiary that obtained MiCAR authorization from the Central Bank of Ireland. This allows it to provide compliant fiat to stablecoin services throughout the European Economic Area.

This shift is accompanied by the rollout of the Aave App, a mobile savings application offering yields significantly above traditional finance while abstracting all on-chain complexity. Deposits can be made via bank account, card or stablecoins, with the backend powered by the Aave protocol and eventually the GHO stablecoin.

Aave now positions itself across three pillars: Aave Protocol for DeFi, Horizon for institutions and Aave App for retail. This aligns the protocol fully with the emerging on-chain neobank narrative and leverages its structural advantage in redistributing on-chain yield to mainstream users through a regulated interface.