What is HIP-4 and how do Hyperliquid’s outcome markets work?

Published on

Discover how HIP-4 is transforming Hyperliquid into a true infrastructure for non-linear payoff markets, far beyond simple prediction markets. Outcome market architecture, discontinuous payoffs, unified portfolio margin, new on-chain financial instruments: this analysis explores why HIP-4 could open a new chapter in the history of on-chain trading.

Introduction

In just two years, Hyperliquid has proven that it is still possible to innovate, build, and distribute an on-chain finance product that actually works, attracts users, generates revenue, and competes with centralized giants. As simple as that may sound, it is still a major breakthrough for this industry.

At the beginning of last year, we published our thesis on Hyperliquid’s vision, which we described as the “AWS of liquidity.” Just as AWS revolutionized cloud infrastructure by abstracting away technical complexity and letting developers focus on building products, Hyperliquid has done the same thing for liquidity.

The real success of Hyperliquid is not just the quality of its product, execution, or tokenomics. Above all, it comes down to one key point: building a high-performance infrastructure capable of attracting and retaining liquidity. Hyperliquid’s true competitive advantage is its ability to transform liquidity into a resource accessible to everyone.

Every layer of Hyperliquid’s development proves this point. Builder Codes are based on a simple idea: instead of acquiring users through traditional channels, product distribution is outsourced to any third-party application that wants to offer trading services to its users by simply connecting to Hyperliquid’s infrastructure.

Following the same logic, HIP-1 introduced native spot assets and their associated order books. HIP-2 created liquidity bootstrap mechanisms. HIP-3 materialized Hyperliquid’s thesis by making perpetual market creation permissionless for external deployers while leveraging the most performant and liquid infrastructure in the market.

HIP-4 follows the exact same path. It introduces a new category of markets that is still relatively unknown in on-chain finance, bringing a new form of payoff and opening a new playground for deployers and builders who will handle distribution and monetization while Hyperliquid continues monetizing its infrastructure in the background.

Today, traditional financial markets are largely dominated by products with non-linear payoffs: options, CDS, insurance products, structured products, and more. A huge portion of this market surface has so far been absent or barely represented in on-chain finance.

HIP-4 is essentially Hyperliquid’s attempt to fill that gap by integrating outcome markets directly into a financial infrastructure that already supports spot and perpetual markets, while replicating the same deployment logic that made previous HIPs successful.

Start Trading on Hyperliquid

Trade 100+ perps with up to 40x leverage on a fully decentralized exchange.

What is HIP-4?

General overview

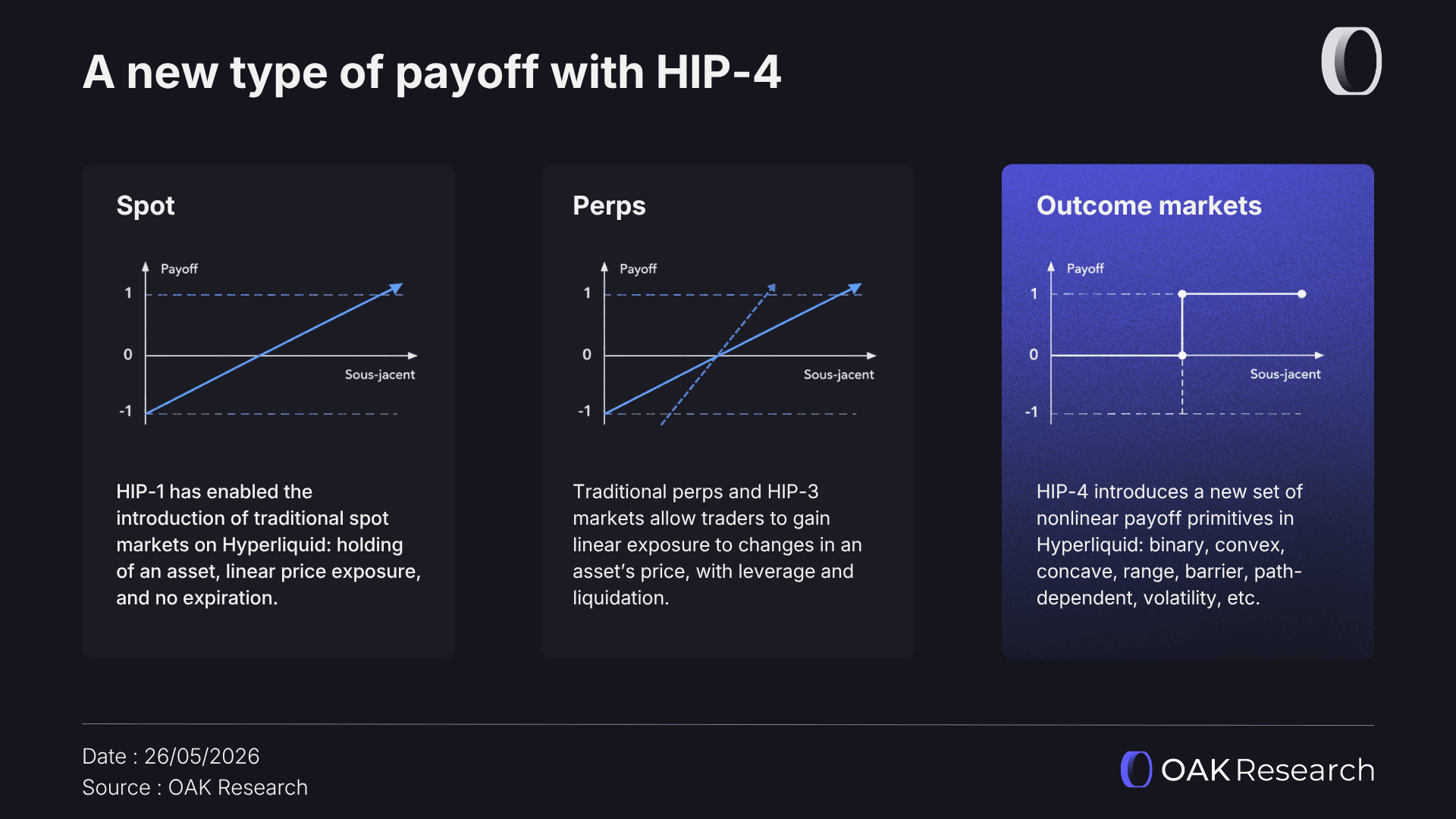

HIP-4 is a new primitive introduced by Hyperliquid called “outcome markets.” These are fully collateralized financial contracts that settle within a predefined price range and whose final value depends on whether a specific event occurs. They can be compared to prediction markets or to instruments similar to bounded options.

An outcome market works according to a simple structure. A question about a real-world event is defined, an expiration date is set, a resolution condition is specified, and the market gradually converges toward a final value between 0 and 1.

In its simplest form, an outcome market functions as a binary market. Two positions exist: YES and NO. If the event occurs, the YES token settles at 1 USDC while the NO token settles at 0. If the event does not occur, the opposite happens. Before final settlement, contracts trade freely on separate order books while remaining linked through negate and merge operations, allowing them to share liquidity.

The price of YES and NO tokens directly reflects the implied probability assigned by the market to the event occurring. If the YES token trades at a price P, the NO token will mechanically trade at 1-P. This mechanism ensures mathematical consistency between both outcomes at all times (YES + NO = 1).

The first HIP-4 market deployed on Hyperliquid illustrates this mechanism clearly. The question is: “Will BTC close above ___ $ at 06:00 UTC tomorrow?” A trader buying YES at 0.62 USDC is therefore paying 62 cents for a potential 1-dollar payoff if the event occurs. If BTC closes below the specified price, the contract expires at 0 and the maximum loss is simply the initial amount committed.

At first glance, the structure looks relatively similar to traditional prediction markets like Polymarket or Kalshi. However, the difference is fundamental: HIP-4 outcome markets are not designed as consumer-facing applications whose goal is to offer as many viral markets as possible with the most intuitive front-end. In reality, they are designed to provide Hyperliquid with a new category of financial instruments that complements its existing offering.

Outcome market architecture

From an architectural standpoint, HIP-4 is natively integrated into HyperCore. This means outcome markets share the same CLOB infrastructure, matching engine, order types, and performance as spot and perpetual markets. We are talking about a theoretical capacity of 200,000 orders per second with finality in less than one block. No separate system, no parallel infrastructure, and no migration required.

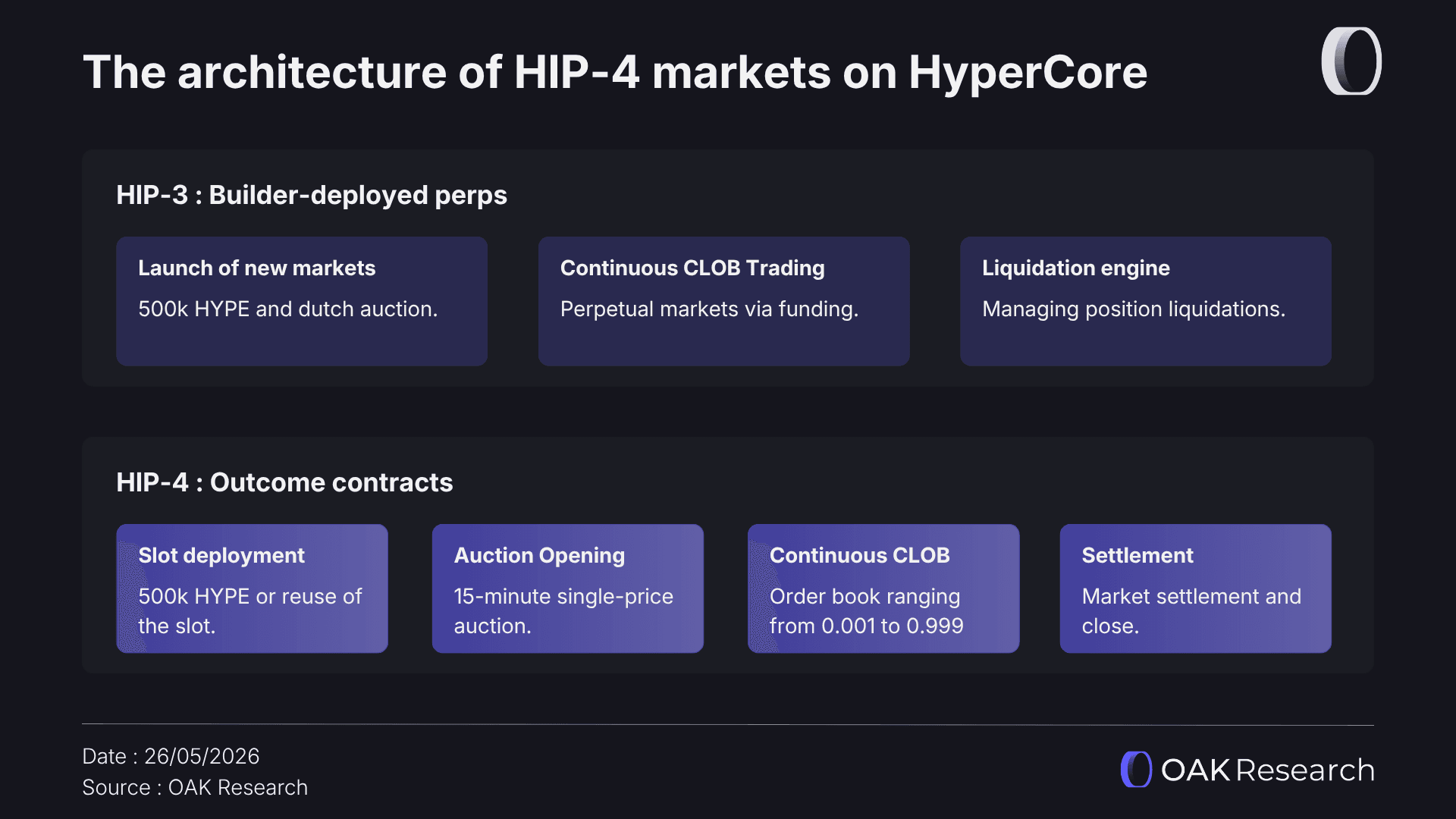

Concretely, a market is created through an OutcomeDeploy request defining several key parameters: the resolution condition, expiration date, settlement source, collateral asset, and the authorized broadcaster allowed to post the final market result. This architecture is directly inherited from the foundations introduced by HIP-3.

This means a HIP-3 deployer can launch an outcome market using the same deployment slot and the same 500,000 HYPE stake. The outcome module is simply an additional parameter in the request: including it creates an outcome market, omitting it creates a standard perpetual market. Deployers already active within the HIP-3 ecosystem can access HIP-4 without any additional steps.

The lifecycle of a HIP-4 market unfolds in four phases:

- The first phase is market deployment with all parameters defined.

- The second phase is the auction opening, lasting around 15 minutes, using a single-price auction that collects orders without immediate execution before settling at an equilibrium price. This phase is critical for initial price discovery on markets with no trading history.

- The third phase is continuous trading on the shared YES/NO order book until expiration. Notably, the transition from phase 2 to phase 3 occurs through migration of remaining auction orders into the continuous order book.

- The fourth and final phase is settlement. The authorized broadcaster posts the final value, the protocol automatically resolves positions, and USDC is distributed to holders on the winning side.

The documentation also introduces the concept of “Questions.” These are outcome markets with multiple outcomes where exactly one settles YES and all others settle NO. This mechanism enables multinomial markets such as: “What will U.S. inflation be next June?” with multiple possible outcomes (<3.3%, <3.4%, <3.5%, etc.).

The merge and negate mechanisms between order books maintain coherent relationships between implied probabilities while avoiding unnecessary liquidity fragmentation across independent markets.

Other important points

- Risk management, collateralization, and settlement:

Before HIP-4, Hyperliquid operated with a continuous risk engine designed for perpetual markets. Outcome markets follow a completely different logic: since the payoff is bounded from the start, the maximum risk of a position is immediately known at trade execution. A trader buying a YES contract at 0.62 USDC can never lose more than 0.62 USDC nor gain more than 0.38 USDC.

This property may sound simple, but it introduces a major shift in risk management and settlement mechanics. HIP-4 positions are fully collateralized at creation, eliminating a large portion of the complexity. No aggressive liquidation engine is required because the protocol already holds the maximum potential loss from both sides of the market.

- Discontinuous payoffs:

This is the key feature mentioned above that allows Hyperliquid to introduce significant flexibility in payoff design. While spot and perpetual markets have linear payoffs (the more the underlying asset price rises, the more your position gains increase linearly), HIP-4 introduces a broad range of non-linear payoffs (binary, convex, concave, range, barrier, path-dependent, etc.), which we will discuss in more detail later in this article.

- HIP-4 deployment roadmap:

We are currently in phase 1 of HIP-4 markets. This phase is intentionally controlled and limited to “canonical” markets launched only by the Hyperliquid team. The goal is to ensure early markets function properly without payoff, settlement, or condition issues.

Phase 2, expected soon, will open permissionless deployment to all builders. It introduces slot recycling: a mechanism where a single 1 million HYPE stake supports a rolling series of markets over time. This incentivizes deployers to create recurring markets (daily BTC markets, earnings releases, Fed meetings, etc.) rather than temporary viral markets.

- An aggressive fee structure:

Opening or minting a HIP-4 position is free. Fees follow HyperCore’s spot fee schedule (7 bps taker / 4 bps maker) and only apply on closing or settlement. A SetOutcomeFeeScale parameter allows fees to be adjusted specifically for prediction markets, though they are currently set to zero for canonical markets.

Compared to Polymarket, which charges up to 2% on winning positions, or Kalshi’s tiered fee model that accumulates for active traders, the difference is currently highly favorable.

- Portfolio margin integration:

HIP-4 positions integrate directly into Hyperliquid’s portfolio margin system. They coexist within the same account and share the same USDC collateral as spot and perpetual positions. Volumes generated by outcome contracts also count toward overall account fee tiers.

The three payoff dimensions of HIP-4

Most commentary around HIP-4 still presents outcome markets as a simple extension of traditional prediction markets. That interpretation is relatively reductive because it confuses the visible use case with the actual financial primitive Hyperliquid is introducing.

Hyperliquid explicitly describes HIP-4 as useful for “applications such as prediction markets and instruments similar to bounded options.” The second part of that sentence is the most important. Prediction markets aim to create markets around viral events to drive speculation, while outcome markets aim to introduce a new payoff primitive to Hyperliquid.

A HIP-4 outcome contract can be configured across three independent dimensions, and the combination of these dimensions defines the final product. Let’s break down what this means.

Settlement input

The first dimension is what the market measures. This can be an asset price, an interest rate, a spread between two assets, an on-chain metric such as TVL or protocol revenue, a protocol state (exploit, depeg, upgrade), macroeconomic data, or any external data verifiable by an authorized broadcaster.

This is not limited to crypto prices, nor to public-facing events. A market could settle based on the average funding rate of a perpetual market over a week, the ratio of liquidations triggered during a session, or a company’s earnings per share. Anything that can be objectively observed and verified is a valid settlement input.

This flexibility is fundamental because it transforms HIP-4 into risk representation infrastructure rather than just another directional market. As soon as data can be objectively defined and resolved through an identifiable settlement source, it potentially becomes usable inside an outcome market.

Observation mode

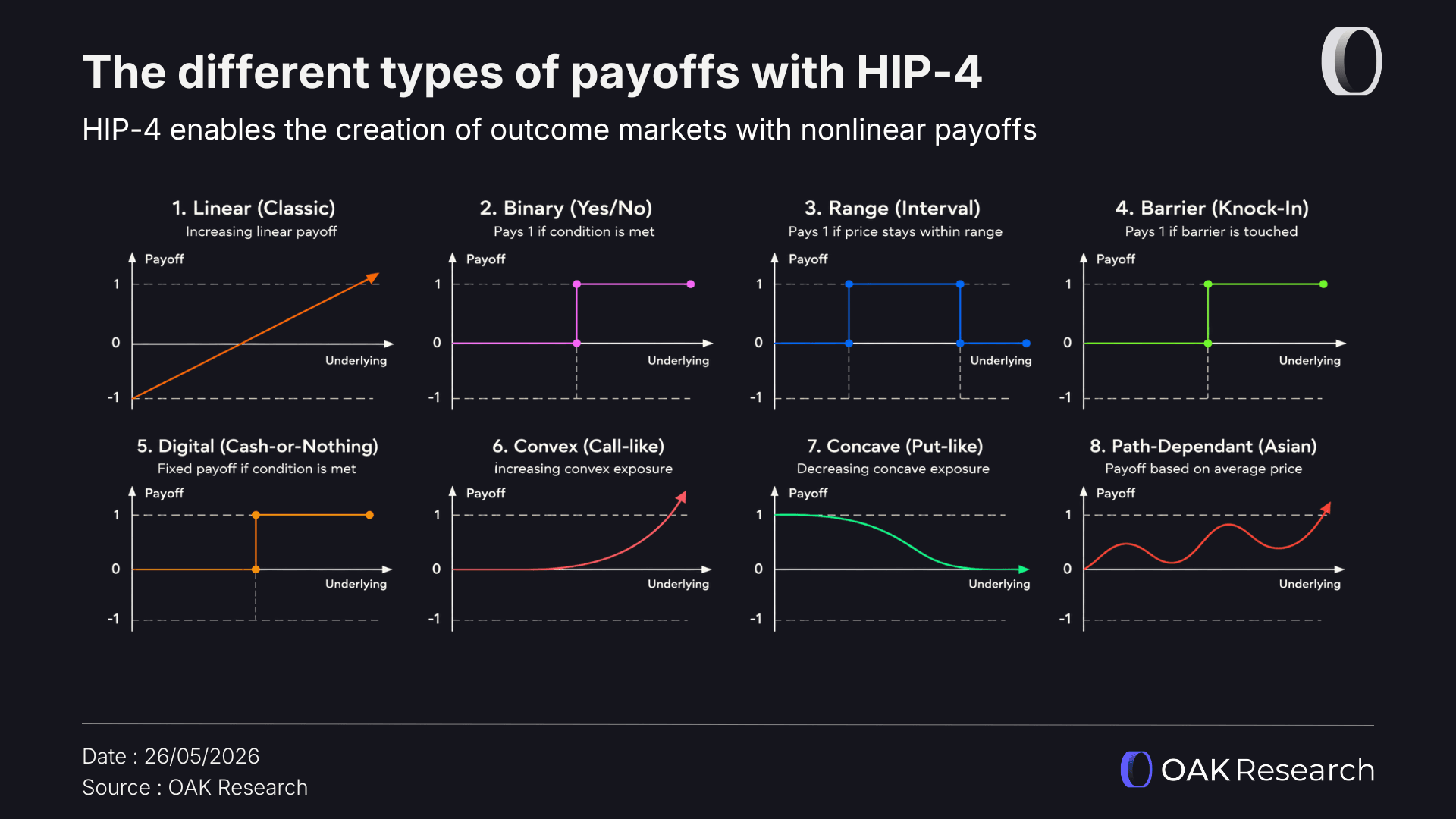

The second dimension defines how that input is measured. The value can be observed at exact expiration, across a time window, based on the maximum or minimum reached during the period, based on how long a threshold was exceeded, or simply whether a threshold was touched at any point during the observation window.

This dimension dramatically expands the number of use cases. A market asking “Will BTC be above 100k at expiration?” and another asking “Did BTC touch 100k at least once this week?” are two entirely different products with different risk profiles, probabilities, and trader use cases.

In the first case, only the final value matters. In the second, the market becomes path-dependent, meaning that simply crossing the threshold at any moment is enough to trigger the payoff.

Yet both products are built on the same primitive, with the same settlement input and only a different observation mode. This is the strength of HIP-4: the ability to open the infrastructure to entire families of traditional derivatives such as barrier options, range options, and certain exotic structured products.

Payoff shape

The third dimension is the most important: the payoff function itself. This is what defines how the observed outcome gets transformed into economic value for contract holders.

In the first HIP-4 markets, this function is binary. The contract settles at either 0 or 1 depending on whether the event occurs. However, this structure is just an extremely basic form of discontinuous payoff.

As a reminder, spot and perpetual markets rely on linear payoffs because gains evolve linearly relative to changes in the underlying asset price. By contrast, finance contains a huge variety of non-linear payoffs: binary, convex, concave, range-based, barrier, path-dependent, volatility-linked, and more.

HIP-4 introduces the possibility of integrating entirely new payoff structures into Hyperliquid. One could imagine scalar payoffs where the final value is a continuous function of the observed result, range-based payoffs where the payout is maximized if the result falls within a predefined range, or composite payoffs built from multiple legs.

With HIP-3, deployers gained control over market creation (deciding which markets are tradable). With HIP-4, they now gain control over payoff construction itself (deciding how claims resolve). These are no longer simply new assets. They are entirely new forms of tradable risk.

Why HIP-4 was necessary for Hyperliquid

Massive demand, but no real on-chain offering

Before explaining what HIP-4 structurally changes for prediction markets, it’s important to start with a simple observation: instruments with non-linear payoffs represent a massive part of traditional financial markets, yet they remain extremely underdeveloped in on-chain finance.

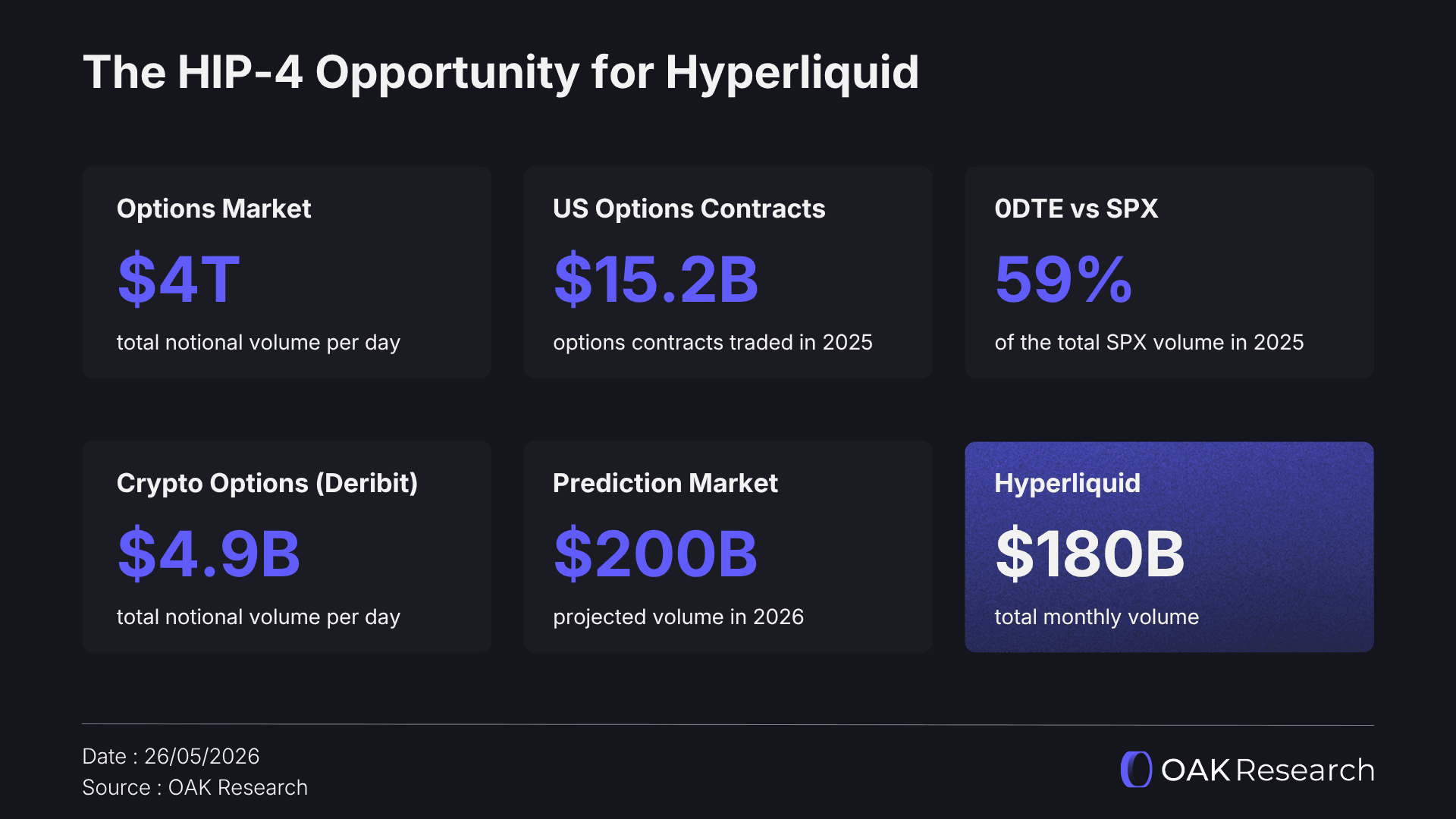

Options markets are the most obvious example. Cboe reported that 2025 marked the sixth consecutive record-breaking year for listed U.S. options, with total volume surpassing 15.2 billion contracts and an average daily volume of 61 million contracts. Zero-days-to-expiration options (0DTEs) alone represented 59% of SPX volume, averaging 2.3 million contracts per day.

On the crypto side, Deribit dominates the options market with $1.875 trillion in 2025 volume and more than 85% market share. It is a centralized, off-chain platform structurally disconnected from on-chain liquidity. Prediction markets reached $63.5 billion in volume in 2025, compared to $15.8 billion in 2024, with the 2026 run rate annualizing around $250 billion.

All of these markets share one fundamental characteristic: they allow users to express views on future states of the world rather than simply taking directional exposure on an asset price. And all of them remain either absent or heavily fragmented on-chain, despite the fact that demand clearly exists given their success in traditional finance.

This is precisely the missing piece of on-chain finance. At least, until HIP-4 arrived. That is why we believe HIP-4 is less about Hyperliquid expanding into prediction markets, and more about solving a major unmet need for traders.

The major limitation of perpetuals

Before HIP-4, HyperCore essentially offered two major forms of exposure. Spot markets allowed users to hold an asset directly, with a linear payoff proportional to price movements. Perpetuals provided leveraged directional exposure, but their payoff structure remained fundamentally linear as well.

For a perpetual market to function properly, it requires three inseparable components: a continuous oracle tracking the underlying asset price in real time, a funding rate mechanism that maintains convergence between the perpetual and spot price, and a liquidation engine managing leveraged positions. This architecture works perfectly when the underlying asset is liquid, continuously priced, and observable at all times.

However, this structure becomes far less suitable once applied to discrete events. The question “Will BTC close above $100,000 on Friday?” is not an asset with a continuous price. As expiration approaches, the market price no longer tracks a continuously evolving underlying asset, but rather a probability that must suddenly converge toward either 0 or 1. There is currently no natural continuous oracle for this type of market.

This discontinuity makes market making significantly harder, increases arbitrage risks between order books, and can even create absurd situations where perfectly solvent positions become difficult to manage using an engine designed for continuous pricing environments. In other words: it is impossible to force this structure into the perpetual model.

HIP-4 also serves as a technical solution to the reality that perpetual markets and HIP-3 were simply not designed to support financial instruments with non-linear payoffs. Once again, HIP-4 should be understood as an extension of Hyperliquid’s capabilities.

Become Premium

Unlock all our research and get the right insights, at the right time.

What HIP-4 changes for prediction markets

The next step is risk markets

Quite naturally, HIP-4 markets are often compared to products offered by Polymarket or Kalshi. In reality, we believe HIP-4 represents the next stage in the natural evolution cycle of prediction markets. Concretely:

- The first phase in prediction market history was the era of “Information Markets”: tools designed to aggregate information and produce probabilities more efficiently than polls, experts, or traditional forecasting models.

- The second phase is the era of “Speculation Markets”: the phase we are currently in, where users transform opinions into bets on real-world events through simple, intuitive, speculation-driven platforms.

Polymarket perfectly embodied this second phase. The platform demonstrated that prediction markets could become consumer products, attract users, generate valuable signals, and become a reference point for forecasting major events such as U.S. elections. But that success does not necessarily mean the current format is the final form of the sector.

- The third phase is the era of “Risk Markets”: at this stage, markets no longer exist purely for prediction or betting. Instead, they become tools for creating new forms of financial exposure to specific risks. The goal becomes using real-world events as a new way to trade either directionally or as a hedging instrument.

This is exactly what HIP-4 enables. Not by building a better prediction market interface than what already exists, but by integrating outcome contracts into the same infrastructure as perpetuals, spot markets, and HIP-3 markets. For the first time, a trader can think of an outcome market not as an isolated bet, but as part of an integrated portfolio strategy.

The distinction matters. A traditional prediction market is something users visit to speculate on an event. A “risk market” is an instrument integrated into portfolio construction and risk management strategies. HIP-4 clearly pushes outcome markets toward this second category.

Unified margin as the fundamental breakthrough

One of the most interesting and probably most underestimated aspects of HIP-4 is its integration into Hyperliquid’s portfolio margin system. Yet this is essential for understanding why outcome markets can become something far beyond simple prediction markets.

Portfolio margin unifies spot and perpetual accounts to improve capital efficiency while also enabling yield generation on eligible idle assets through the “earn” function (primarily USDC for traders).

Polymarket operates with isolated positions: capital deployed into one market is fully siloed from the rest of the user’s portfolio. A position on Market A cannot serve as collateral for a position on Market B. Even worse, users cannot hedge a Polymarket position with a perpetual position elsewhere.

Hyperliquid solves this issue because a HIP-4 outcome contract can coexist within the same account as spot and perpetual positions. The same collateral can therefore support both a long BTC position and a NO position on “Will BTC exceed ___ $ tomorrow?” This dramatically improves capital efficiency for traders as well as market makers.

This last point is extremely important because market makers struggle to operate efficiently on platforms like Polymarket or Kalshi due to their technical structure. On Hyperliquid, they can easily hedge HIP-4 market-making strategies through spot or perpetual positions.

Additionally, this opens massive possibilities for builders, who can now create structured products combining directional perpetual exposure with conditional payoffs within a single interface. This is exactly what the “Risk Markets” phase requires: instruments capable of integrating into broader portfolio logic, collateral efficiency, and dynamic risk management.

Fewer markets, better defined, more liquid

Another major difference between HIP-4 and current prediction markets is the logic behind market creation and curation. Platforms like Polymarket and Kalshi benefit from listing as many markets as possible to maximize engagement, virality, and social media coverage. This works perfectly for a business model centered around speculation and consumer entertainment.

Hyperliquid has no incentive to replicate this model. The economics of HIP-4 naturally push toward recurring, standardized, highly liquid markets that are attractive to traders. In other words, the logical outcome should be an ecosystem with fewer markets, but markets that are more integrated with existing tradable assets because the goal is to turn outcome markets into actual financial instruments.

Additionally, slot recycling will likely incentivize deployers to optimize a single slot around recurring high-potential markets rather than fragmenting liquidity across an illiquid long tail. An illiquid market that cannot scale is not a useful risk management tool. A recurring market with clear settlement, sufficient depth, and native integration into margin accounts can become one.

The cold start advantage

Prediction markets suffer from the same core problem that affects much of on-chain finance: liquidity. No liquidity without market makers, no market makers without volume, no volume without users, and no users without liquidity. It is a vicious cycle that Polymarket eventually managed to break after several years, largely thanks to the major catalyst of the U.S. elections.

HIP-4 starts with a huge advantage: an existing base of active traders, professional market makers, deep liquidity, and ultra-performant infrastructure. Market makers, builders, and deployers are already connected to Hyperliquid and can distribute HIP-4 markets without rebuilding an entire trading infrastructure from scratch.

This does not guarantee HIP-4 will succeed. But it fundamentally changes the typical “cold start” problem most protocols face. This is probably one of Hyperliquid’s biggest advantages: it does not need to bootstrap liquidity from zero.

Infrastructure versus consumer business

The comparison between Hyperliquid, Polymarket, and Kalshi is inevitable, but it is often framed incorrectly. Polymarket and Kalshi are fundamentally “consumer distribution businesses.” Their edge comes from branding, user experience, regulatory positioning, media attention, and in Kalshi’s case, a clearer regulatory framework within parts of the U.S. market.

Hyperliquid operates under a completely different logic. HyperCore is not necessarily trying to become the best retail-facing prediction market interface. Its value proposition is to provide the execution, margin, and liquidity infrastructure on top of which other players can build products.

That is why lower fees alone may not be enough to attract Polymarket’s retail user flow directly. A user betting $50 on an election does not necessarily choose a platform based on a few basis points of fees. But for active traders, market makers, or builders, the difference between an expensive, isolated, non-composable infrastructure and a native, liquid, integrated infrastructure becomes extremely meaningful.

As this entire section should make clear, the primary value of HIP-4 lies in creating a new trading primitive for users, improving capital efficiency, and opening new monetization opportunities for builders. This is exactly the logic behind the “AWS of liquidity” thesis we developed around Hyperliquid’s vision.

Risks for HIP-4 and Hyperliquid

Resolution risk

The first major risk around HIP-4 is obvious: an outcome market is only as reliable as its resolution process. A market such as “Will BTC trade above $100,000 at 06:00 UTC tomorrow?” is relatively straightforward to settle. The source is clear, the timestamp is precise, and the outcome leaves little room for interpretation.

This is likely why Hyperliquid is initially focusing on canonical crypto-native markets based on objective and easily verifiable data sources. This approach reduces dispute risk during the early stages and allows the infrastructure to be tested on simpler markets.

The permissionless phase will be significantly more challenging. Deployers will need to define their own markets, choose their own data sources, write settlement conditions, and manage edge cases. The more markets rely on subjective or difficult-to-measure events, the higher the dispute risk becomes.

In outcome markets, trust is not a secondary layer. It is the product itself. A poorly resolved market can create reputational contagion far beyond the market directly affected.

Regulation

Prediction markets remain a highly sensitive regulatory category. Depending on the jurisdiction, they may be treated as financial products, gambling instruments, event contracts, or derivatives. Polymarket, Kalshi, Crypto.com, Robinhood, and Coinbase have all already faced various forms of regulatory pressure around these issues.

For Hyperliquid, the risk profile will depend heavily on the types of markets allowed on HIP-4. As long as markets remain crypto-native, objective, and tied to financial data, the regulatory risk appears more manageable. It becomes significantly more complex if the ecosystem expands into politics, sports, or highly sensitive macro events.

The permissionless structure adds another layer of complexity. Hyperliquid may provide the infrastructure, but deployers and builders will likely play a critical role in curation, distribution, and compliance depending on the jurisdiction.

Information asymmetry

Outcome markets naturally create financial incentives for actors with privileged information. This is a structural tension within the model itself. Their strength comes from aggregating dispersed information, but that same property makes them attractive to participants holding non-dispersed information.

This issue already exists in current prediction markets. Actors with faster access to data, insider information, or superior analytical capabilities can capture a disproportionate share of profits. This is not always illegitimate, since markets are fundamentally designed to reward information. But once that information becomes privileged, confidential, or improperly obtained, the nature of the risk changes entirely.

On-chain transparency may help detect certain behaviors after the fact, but it does not prevent them. As HIP-4 expands into more sensitive markets, surveillance, market rule quality, and resolver accountability will become critical components of the system.

The quality problem of the long tail

Permissionless deployment is a strength, but it can also generate noise. Poorly designed, illiquid, redundant, or badly resolved markets can degrade the overall quality of the ecosystem. This risk is especially important for outcome markets because poorly defined markets create more than just a bad user experience: they can create disputes.

The economic viability of deployers will therefore likely depend as much on controlling market quality as market quantity. A good outcome market must be interesting, liquid, clearly defined, easy to resolve, and recurring enough to justify the attention of traders and market makers.

This is where Hyperliquid’s structure may create an advantage. Slot recycling and HyperCore integration naturally incentivize the creation of recurring, economically useful markets rather than an infinite long tail of illiquid questions. However, this incentive alone will not completely eliminate the risk of spam or poor curation.

Conclusion

HIP-4 is not simply Hyperliquid’s response to Polymarket. It is a new primitive added to HyperCore, directly aligned with the trajectory the protocol has followed since launch.

HIP-1 introduced native assets. HIP-2 strengthened liquidity. HIP-3 enabled permissionless perpetual market creation. HIP-4 now opens the door to discrete, conditional, and non-linear payoff markets. Each step follows the same logic: expanding the range of markets available on HyperCore while keeping the same execution engine, liquidity layer, and distribution infrastructure.

For prediction markets, HIP-4 likely represents the transition we described in the previous article: the evolution from Information Markets to Speculation Markets, and gradually toward Risk Markets. At this stage, markets no longer exist purely for prediction or betting. They become financial instruments designed to open, hedge, or transfer exposure to event-driven risk.

This is precisely what differentiates Hyperliquid from Polymarket or Kalshi. Those platforms remain primarily consumer distribution businesses built around attention, curation, and user acquisition. Hyperliquid is building financial infrastructure where these markets can become composable with the rest of on-chain trading.

The real question is therefore not simply whether Hyperliquid can capture a portion of existing prediction market volume. The real question is whether HIP-4 can create an entirely new category of markets: fewer in number, better designed, more liquid, and ultimately far more useful for traders looking to manage risk seriously.

Subscribe to Blocknote

Your weekly crypto digest delivered directly to your inbox.