Strategy: Is the “Infinite Money Glitch” Model Sustainable?

Published on

Michael Saylor and Strategy have initiated an unprecedented movement around Bitcoin, built on a model that is often misunderstood and increasingly questioned. This analysis dives deep into how the model works, its financing mechanisms, its risks, and its long-term sustainability. A must-read to understand Bitcoin Treasury Companies.

This article is taken from our 2025 year-end report, produced in collaboration with Castle Labs and Hazeflow. 180 pages, 12 analysts, 20 contributors, and an in-depth analysis covering all the major themes that shaped 2025, along with outlooks for 2026. The report is available for free on OAK Research and can also be purchased in a physical format.

We would also like to thank Kraken for their support in the development of this report. We invite you to join them to support our work. Enjoy the read.

Introduction

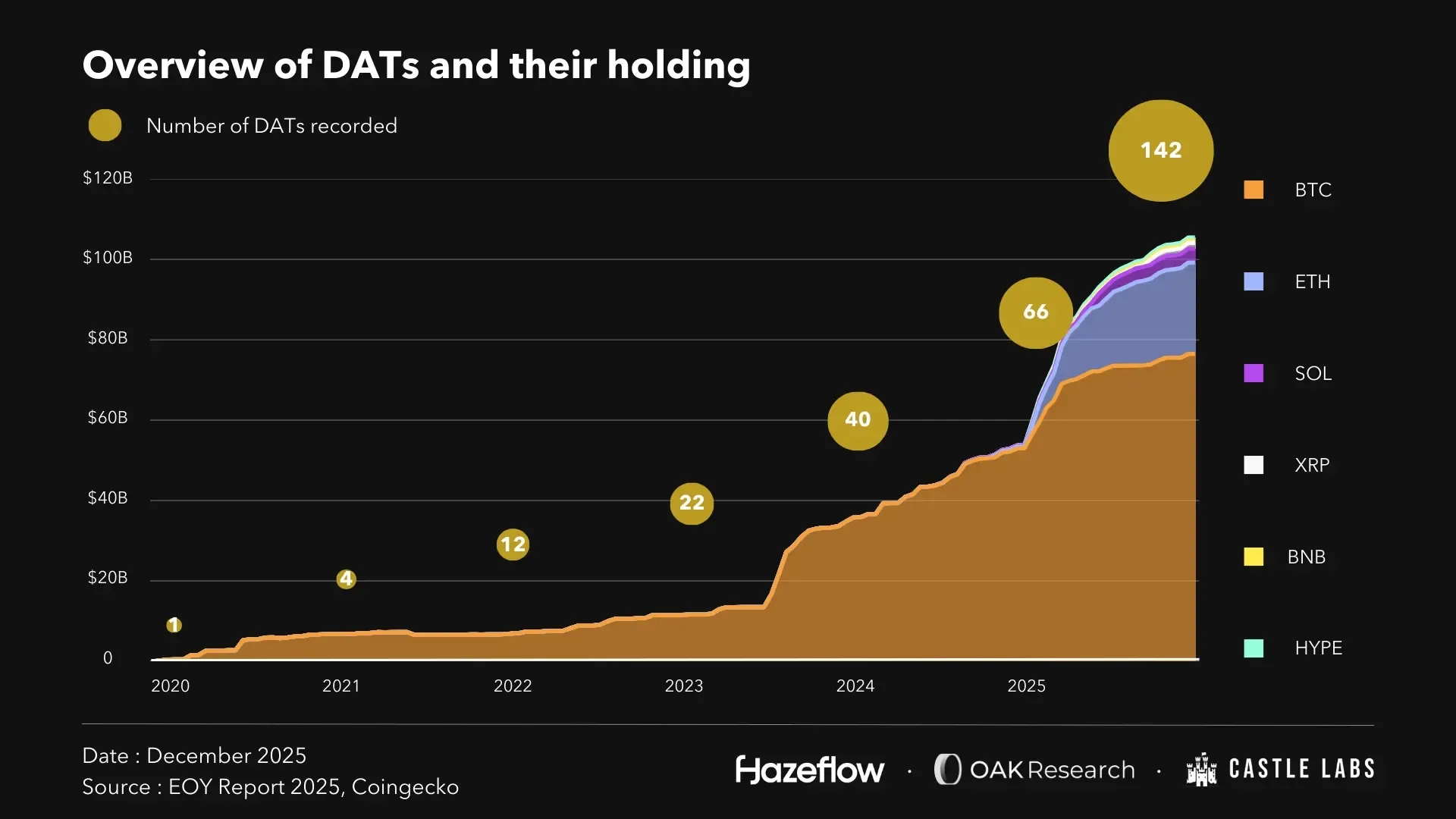

The use of Bitcoin as a corporate treasury asset remains a relatively recent phenomenon, mostly post-2020. At that time, there were only 4 "Digital Asset Treasury Companies" (DATs). By the end of October 2025, that number had risen to 142, of which 113 are directly exposed to Bitcoin, or roughly 80%.

Beyond DATs alone, we are also seeing a rise in listed companies adding BTC to their balance sheets. Today, more than 200 public companies have BTC exposure, and when including private companies, that figure rises to 289.

To date, more than 200 listed companies hold a total exceeding one million BTC, or more than 5% of total supply. This segment is largely dominated by Strategy, which alone accounts for more than 65% of these positions.

If we add private companies (holding 1.33% of supply and driven nearly 90% by Block.one and Tether), the total exceeds 1.3 million BTC. Overall, these entities now hold 6.4% of total supply.

Public companies exposed to Bitcoin fall into three main categories.

- Bitcoin Operating Companies (Strategy, Metaplanet): BTC becomes the central balance sheet asset and the core of the financial strategy.

- Mining companies (MARA, Riot, CleanSpark): "natural" accumulation of BTC through operating activity.

- Tech / industrial companies (Block, Coinbase, Tesla, Nexon): treasury allocation or diversification, without shifting toward a "BTC-first" model.

It is precisely this first category that we will study in this analysis. Bitcoin Treasury Companies, or Digital Asset Treasury Companies more broadly, are now ubiquitous across the crypto ecosystem. Among them, Strategy is the most significant: not only due to the size of its reserves, but above all because of how the company has turned Bitcoin into a driver of funding, yield, and amplification.

In this analysis, we propose to dissect Strategy as a textbook case to understand how other DATs or BTC Treasury Companies work. How the model functions, what makes it sustainable (or not), what the risks are for the company, and what the outlook is for the sector in 2026.

We also interviewed two experts in their fields: Eric Balchunas, Senior ETF Specialist at Bloomberg, to understand the difference between these companies and spot Bitcoin ETFs, and Alexandre Laizet, Board Director of Capital B, the largest Bitcoin Treasury Company in Europe.

From software publisher to Bitcoin-backed financial infrastructure

The starting point (2020)

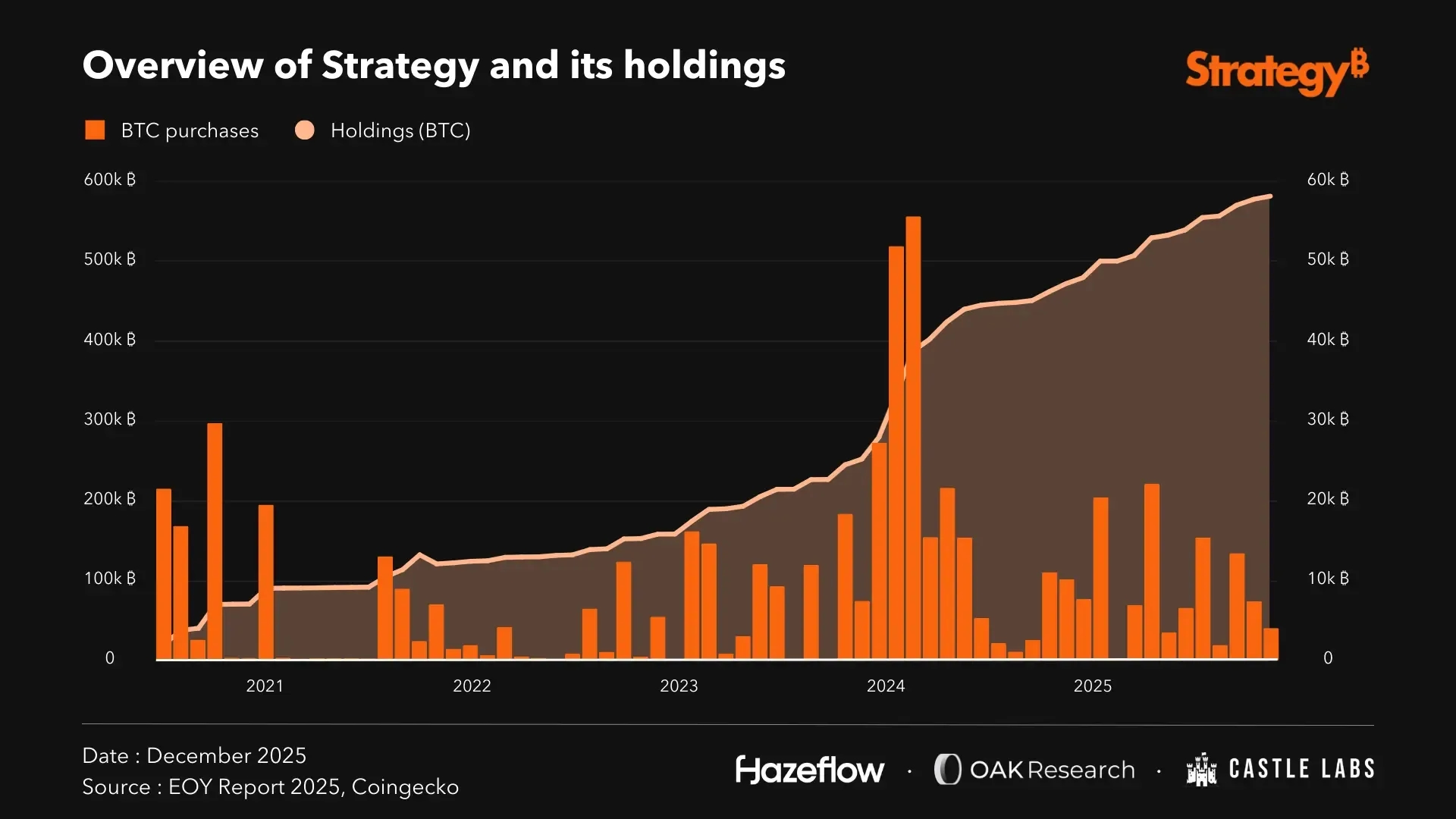

In 2020, MicroStrategy, then a software company, introduced an unprecedented model: turning the treasury of a publicly listed company into large-scale Bitcoin exposure, then amplifying that exposure through capital markets. This pivot is built on a straightforward macro view: cash perceived as structurally low-yielding, and Bitcoin identified as a long-term alternative reserve asset.

In the first half of 2020, MicroStrategy argued that the rate and cash-yield environment was "structurally declining", against a backdrop of macroeconomic risks tied to expansionary monetary policy and expectations of particularly high inflation. In this context, management reassessed the relevance of holding large dollar cash balances and identified Bitcoin as an alternative reserve asset that could preserve, or even improve, purchasing power over the long term.

In August 2020, the company allocated $250 million to purchase 21,454 BTC, formalizing Bitcoin as a reserve asset. Six months later, on December 21, 2020, MicroStrategy announced it held roughly 70,470 BTC at a total cost of $1.125 billion, implying an average cost basis of $15,964. As of December 31, 2020, the carrying value of its "digital assets" was $1.054 billion, including a $70.7 million impairment charge tied to Bitcoin price fluctuations.

The real inflection point came in December 2020 with the issuance of an initial $650 million tranche of convertible notes maturing in 2025. The company was no longer simply allocating existing cash: it was now tapping capital markets to finance a larger-scale Bitcoin accumulation strategy. This deal marked the birth of a new Bitcoin Treasury Company model, where the balance sheet becomes a strategic leverage tool for exposure.

The rebranding pivot (2025)

Between 2020 and 2024, the model gradually expanded, to the point where the historically core software business became increasingly marginal in the firm's overall value creation. In 2025, MicroStrategy formally acknowledged this reality through a full rebrand, becoming "Strategy". Bitcoin was no longer presented as a simple treasury asset, but as the core of the business model.

This identity shift ended the ambiguity that had surrounded the company for years: a firm classified as software, but whose valuation, financial flows, and investor interest depended almost entirely on its Bitcoin exposure. At that stage, less than 3% of revenue still came from the legacy business, while nearly all value creation came from the revaluation of its Bitcoin balance sheet.

In communications to the market, this repositioning is framed as a transition from a "software company with a Bitcoin treasury" to a "Bitcoin Monetary Network Company", meaning a company whose BTC reserve is not only the central asset, but also the economic base underpinning all capital issuance.

Strategy's identity shift also accompanies the gradual move away from debt financing, the rise of perpetual financing, and above all, the redefinition of the corporate mission: accumulate Bitcoin, monetize it through financial instruments, and offer long-duration institutional exposure to Bitcoin.

The "Infinite Money Glitch" strategy?

The convertible debt problem

Between 2020 and 2024, Strategy financed most of its Bitcoin accumulation through a series of bond issuances, primarily senior convertible notes. These instruments served as the first funding lever for the acquisition program, but they gradually introduced a structural constraint: fixed-maturity liabilities backed by an asset held on an indefinite horizon.

By the end of 2024, total outstanding convertible debt reached roughly $7.3 billion, with maturities concentrated between 2027 and 2032, and a pronounced cluster around 2029. This creates a maturity wall that makes the company's financial trajectory structurally dependent on continuous access to capital markets, especially given that the software business no longer generates sufficient cash flows to absorb these maturities on its own.

The mismatch is central: Strategy is accumulating a volatile, non-amortizing monetary asset, Bitcoin, while financing it with mandatory repayment instruments. As long as market access remains smooth and valuation stays favorable, the structure works. But heading into 2025, this constraint becomes the primary limiting factor for the model.

This maturity concentration creates a polarized profile, exposing the company to a structural refinancing risk. The risk is not immediate insolvency, but increasing dependence on market conditions at specific dates. If capital access tightens approaching those maturities, Strategy could be forced to refinance on unfavorable terms or mobilize internal resources, which is incompatible with a long-term accumulation strategy.

In this framework, the ability to keep accumulating depends less on Bitcoin's price than on the depth and stability of access to financial markets. This dependence is a structural fragility for a model designed to operate over decades.

The perpetual financing solution

Starting in 2025, Strategy made a deep shift in the nature of its liabilities. The company progressively replaced maturity-based instruments with perpetual preferred shares, designed to raise capital without any principal repayment date.

The logic is simple: replace fixed-maturity debt with permanent capital compensated by a contractual dividend. This changes the liability profile. The company no longer commits to returning principal, but to compensating capital through a stable stream paid to investors, while taking on volatility and capturing Bitcoin's potential outperformance.

The economic appeal comes from the spread between a fixed coupon paid to preferred holders and the long-term performance of the BTC held on the balance sheet. Distributions are contractually defined and independent of day-to-day volatility, while the company retains any excess return.

In 2025, Michael Saylor referenced an expected annualized return of roughly 29% over the next two decades, a projection built on an annualized return close to 49% over the prior decade.

It is this liability transformation, far more than simply accumulating BTC, that enables what the market has labeled an "Infinite Money Glitch".

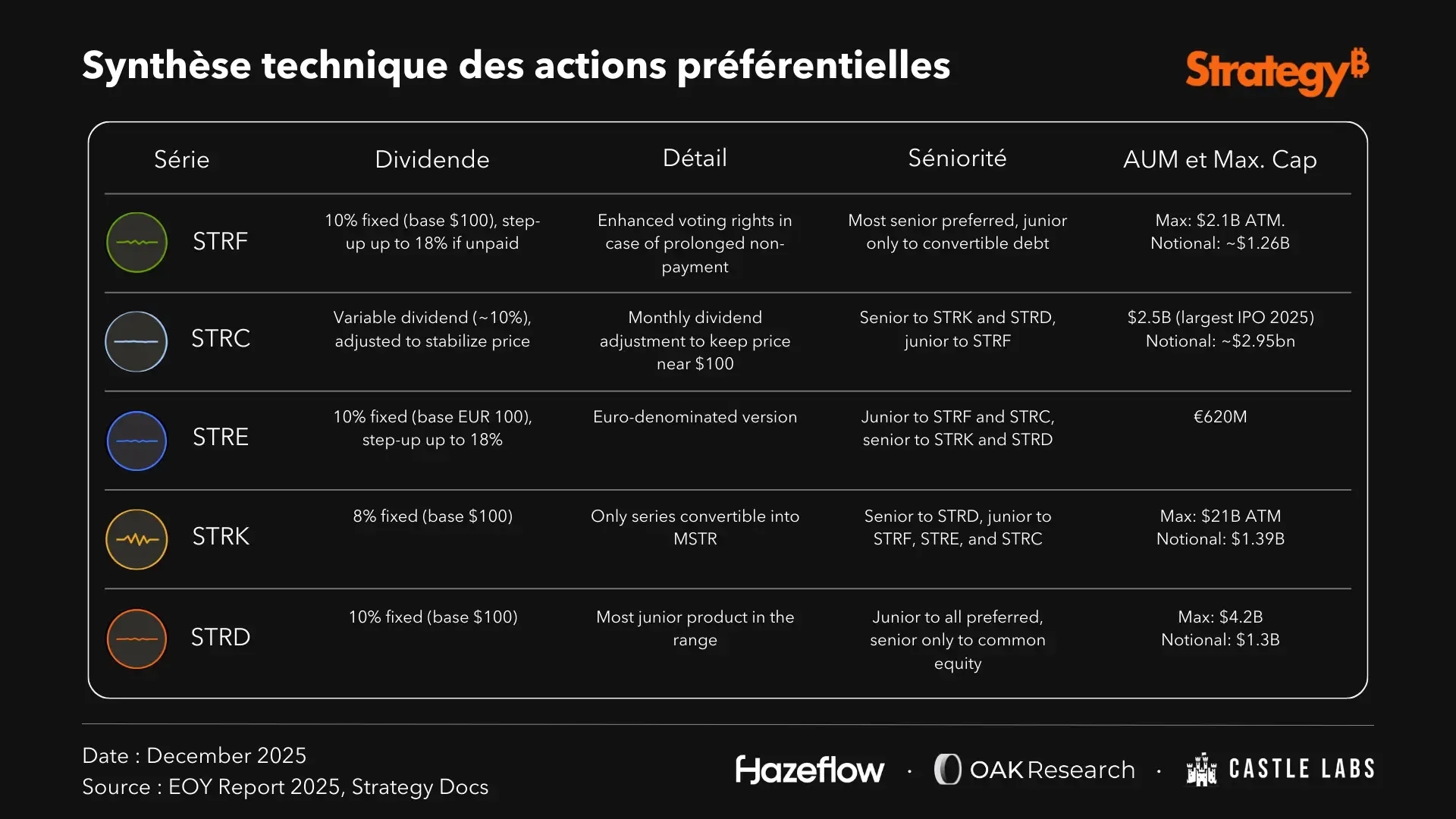

Preferred shares breakdown

The range of preferred shares introduced by Strategy in 2025 is designed to provide the company with a perpetual financing structure, with no maturity, enabling it to raise institutional capital in exchange for a contractual dividend, while deploying those proceeds to increase its Bitcoin reserves.

Each series differs by yield, volatility, seniority, and specific mechanics, enabling the company to target varied investor profiles. All of these instruments are listed on Nasdaq, ensuring continuous liquidity and an oversight framework aligned with U.S. public market standards.

This hierarchy forms a graduated capital structure, where each instrument serves a specific function along the risk-return curve offered to investors. Together, these series allow Strategy to segment institutional demand while maintaining overall financing coherence.

Collectively, these instruments create a Bitcoin-linked yield curve comparable to a bond market, but without maturity and without sovereign collateral. Each issuance strengthens Strategy's ability to raise capital without time pressure, finance Bitcoin purchases, and maintain a capital structure aligned with an asset held over the long term.

This architecture fundamentally differentiates Strategy from a simple Bitcoin-holding company. Value no longer comes only from holding the asset, but from the ability to transform a BTC stockpile into institutional financial flows. As long as market conditions allow it, this structure enables durable amplification of exposure.

Note: another key element of the attractiveness of these preferred shares is their tax treatment. Dividends paid on STRK, STRF, STRD, and STRC are treated as Return of Capital and therefore are not taxed as income, but as a repayment of invested capital. Taxation is deferred until the security is sold or the cost basis is fully recovered. This stems from the fact that Strategy does not generate taxable profit as long as it does not sell its BTC.

Strategy's position at the start of 2026

Consolidated data for Q3 2025 provides a clear snapshot of Strategy's financial position. It confirms three core points:

- A balance sheet now dominated by Bitcoin,

- A mixed capital structure combining convertible debt and preferred shares,

- An atypical operating profile for a company whose primary activity is no longer software, but monetary.

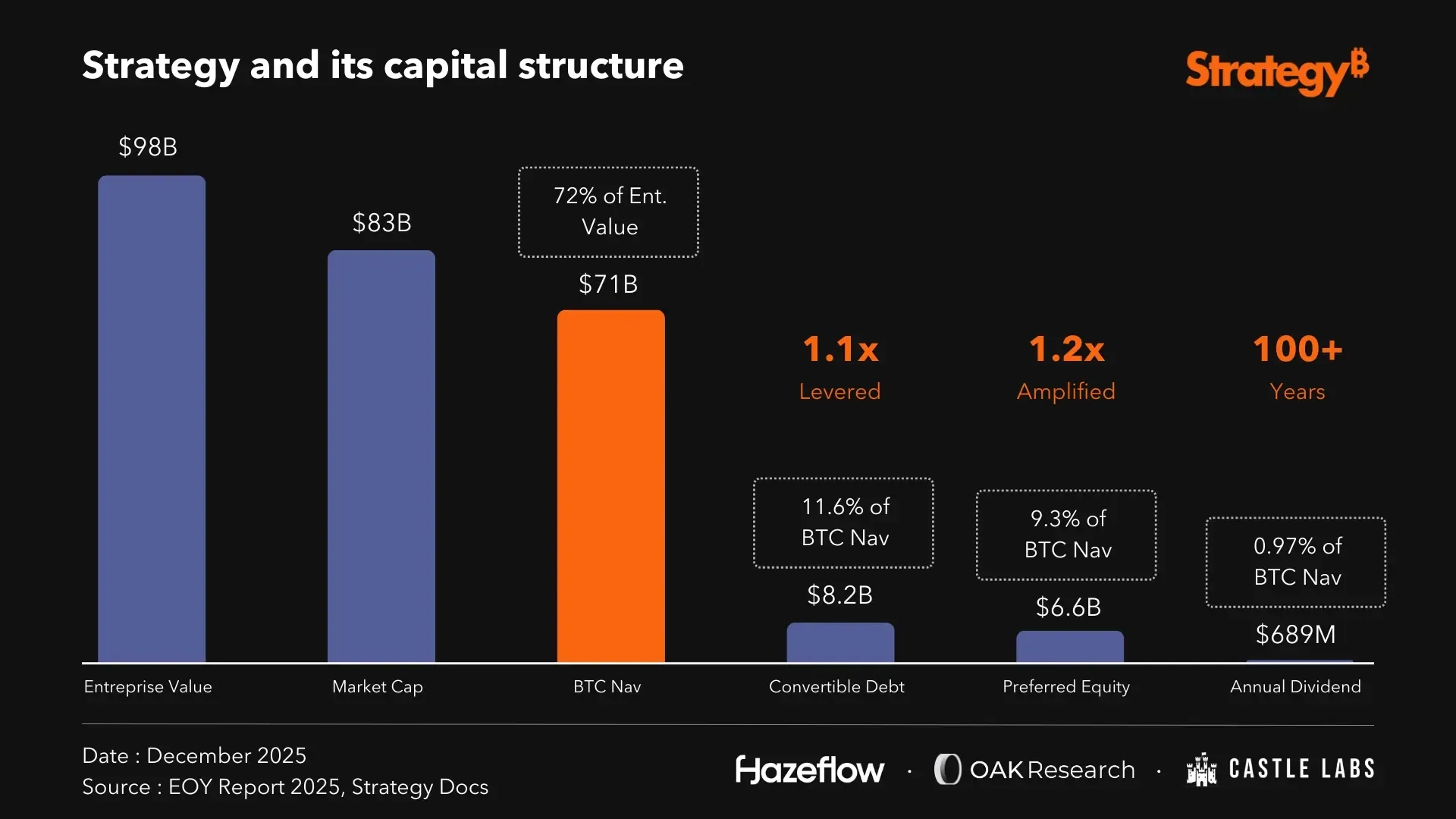

As of end-September 2025, Strategy held 640,808 BTC acquired for a total of $47.44 billion, implying an average unit cost of $74,032. At those levels, the economic value of the Bitcoin reserves (BTC NAV) is around $71 billion, representing nearly three quarters of the company's total value.

Financial leverage remains moderate. Outstanding convertible debt is around $8.2 billion, corresponding to roughly 11% leverage relative to the value of BTC held. Over time, this debt must be converted or repaid, and it conditions part of the company's financial path over 2025-2029.

Preferred shares represent roughly $6.6 billion, or about 9.3% of BTC NAV. Total annual interest and dividend burden is about $689 million, corresponding to a cost of capital of roughly 0.97% of the value of Bitcoin reserves.

Here is the information we have on Strategy's financials:

- In Q3 2025, the company posted operating income of $3.9 billion and net income of $2.8 billion, translating into diluted EPS of $8.42. Obviously, these results are almost entirely driven by the rise in BTC during the period.

- As of January 2026, Strategy records roughly $12.9 billion in unrealized gains on its Bitcoin holdings.

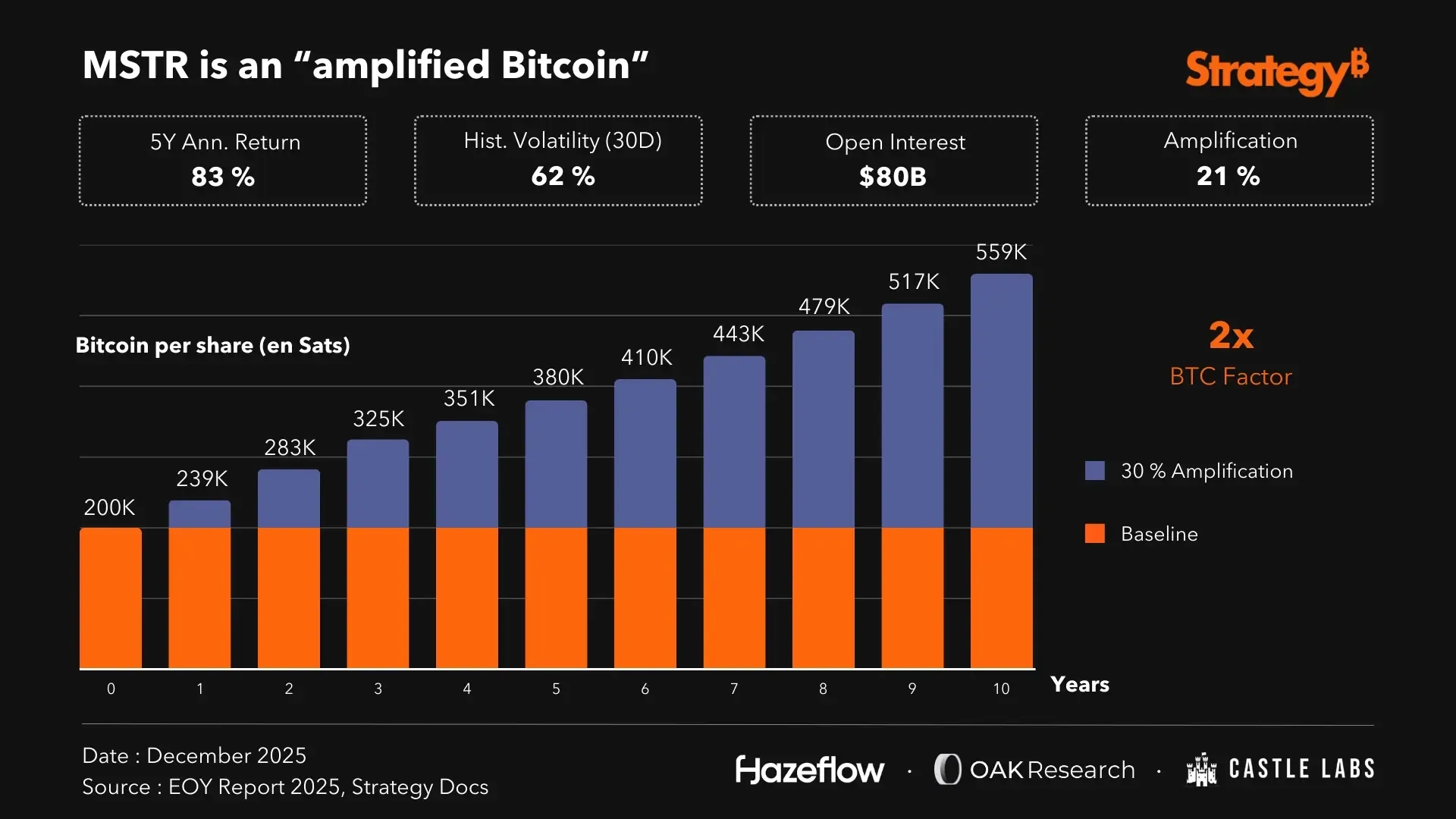

- BTC Yield has now reached 26%. This metric reflects the increase in the number of bitcoins per share and measures the mechanical ability of the model to produce more bitcoins per share year after year.

- Since January 2025, the company has raised nearly $20 billion through its full suite of financial instruments.

Strategy's market communications at the end of October 2025 anticipated net income near $24 billion assuming Bitcoin at $150,000 on December 31. After the November correction, the company revised its projections: for BTC between $85,000 and $110,000, the disclosed range now implies operating income between -$7.0 and +$9.5 billion, and net income that could reach -$5.5 billion in the worst case.

This revision does not invalidate the structural mechanics of the model built on accumulation, amplification, and balance sheet monetization. However, it highlights a major accounting constraint: the fair value standard applied for more than a year now exposes Strategy to immediate volatility in its financial statements.

When Bitcoin falls at quarter-end or year-end, results mechanically shift from positive to negative, without affecting operational capacity, capital structure, or the company's economic solvency.

In other words, the model's economic performance is measured across the cycle, while accounting performance depends on Bitcoin's spot price at the reporting date. Strategy now operates under a much more pronounced "mark-to-Bitcoin" logic than traditional companies, which requires a multi-year reading of its trajectory.

The MSTR premium and the role of mNAV

Definition and mNAV formula

Today, the question investors and, by extension, the market are asking is no longer how many bitcoins Strategy holds in its treasury, but at what price the company's model can fund itself. This is precisely the role of mNAV, which has become the company's central valuation indicator.

mNAV corresponds to the ratio between Strategy's total economic value (enterprise value) and the market value of the bitcoins held on its balance sheet. Unlike a calculation based only on market cap, this approach incorporates the full financial structure: common equity, convertible debt, preferred shares, all adjusted for available BTC cash.

mNAV therefore provides a simple measure of whether the market values Strategy above or below the economic value of its Bitcoin reserves:

- An mNAV of 1 means Strategy's enterprise value is exactly equal to the market value of all its bitcoins.

- An mNAV above 1 (premium) means the market values the company above the simple value of its Bitcoin reserves.

- An mNAV below 1 (discount) means the market values the company below the value of its Bitcoin reserves.

At the end of 2025, Bitcoin's price decline triggered a rapid compression of Strategy's market premium. In this context, the company's USD cash reserve (around $1.4 billion), built via common equity issuance, and an annual dividend/coupon burden estimated around 0.97% of BTC NAV act as a safety cushion that helps ensure payments despite market conditions.

Why mNAV > 1 enables amplification

When mNAV is above 1, Strategy can raise capital at an economic cost lower than the implied value of the Bitcoin represented by each share. In other words, the company issues securities at a price above the economic value of the BTC they dilute, then uses the proceeds to buy additional bitcoins.

This mechanically increases BTC per share, even after dilution. This is not leverage funded by debt, but a valuation premium granted by the market to the structure itself. As long as that premium persists, each issuance strengthens accumulation capacity and fuels the amplification cycle.

Why mNAV < 1 creates stress

When mNAV stays below 1 for a sustained period, the equation flips. Issuing shares becomes value-destructive on an economic per-share basis, because the capital raised buys less Bitcoin than what is diluted. In that regime, amplification via common equity becomes economically inefficient.

The capital structure must then absorb Bitcoin volatility without being able to rely on primary issuance. Access to capital tightens, the marginal cost of new issuance rises, and accumulation capacity mechanically slows. mNAV thus becomes a leading indicator of financial stress in the model, not in terms of immediate solvency, but in terms of the cost of capital.

The risk for MSTR

Common equity issuance increases the total share count and mechanically dilutes BTC per share. Dilution is neutral or value-creative when mNAV is high, because each issued share raises more capital than the Bitcoin "lost" through dilution.

However, when the premium compresses, the balance flips. Issuing at low mNAV or below 1 destroys economic value per share, the capital raised no longer buys enough BTC to offset dilution, and the BTC reserve per share declines. Ultimately, this weakens Strategy's ability to maintain an advantageous accumulation trajectory.

Common shareholders simultaneously absorb Bitcoin volatility and dilution risk from new issuance. This residual role makes MSTR the most exposed instrument in Strategy's structure, the layer that bears all risk after preferred holders are compensated.

Expert view with Alexandre Laizet, Capital B

Once mNAV falls below 1, how can a company continue to raise capital and increase its Bitcoin purchases?

A Bitcoin treasury company is primarily valued by its ability to increase the number of bitcoins per share over time. When mNAV (market net asset value) drops below 1, raising capital only through equity issuance becomes inefficient because it can dilute bitcoins per share. That directly contradicts the company's objective. This is precisely why players like Capital B have developed funding mechanisms based on long-term credit, notably five-year convertible notes denominated in Bitcoin. These allow the company to raise Bitcoin with an embedded premium in the financing instrument, without relying on mNAV premium in the market.

An mNAV below 1 remains a critical indicator of market sentiment. In periods of extreme fear, that sentiment can heavily weigh on investor perception, especially when they face short-term capacity or horizon constraints, even when long-term fundamentals remain strong and conviction is unchanged. In that respect, Capital B draws inspiration from peers such as Metaplanet, which managed to access credit on attractive terms to continue its accumulation strategy, and Strategy, which has historically used various financing tools during bear phases (including when its mNAV was below 1). Today, the latter is developing instruments (like preferred shares) designed to raise capital while minimizing common equity issuance over time.

Finally, equity remains one financing tool among others, but it must be deployed with discipline and care. The use of more sophisticated instruments, such as preferred shares or equivalents, and more broadly the issuance of long-term credit with an embedded premium, illustrates the ability of Bitcoin treasury companies to raise capital even in unfavorable environments. It shows that a robust Bitcoin treasury strategy relies on multiple levers, both equity and credit, to keep creating value over the long term.

The "Flywheel" model and risks

How the model works

Strategy's model is built around a self-reinforcing mechanism linking three key variables: mNAV, capital issuance capacity, and Bitcoin accumulation. As long as mNAV remains above 1, the company can raise capital at an economic cost below the implied value of the Bitcoin it represents, then convert that capital into BTC, mechanically strengthening its balance sheet.

This process helps stabilize, or even increase, BTC per share despite dilution from issuance. It also simultaneously funds dividends on preferred shares, whose cost is contractual and relatively low versus BTC NAV. The increase in the company's value supports the valuation premium in turn, enabling renewed access to capital. This loop is the model's flywheel.

However, the mechanism is entirely conditioned by market perception. A sustained contraction in mNAV or a prolonged Bitcoin drawdown reduces the ability to issue above NAV and forces a slowdown, or even a pause, in amplification. When mNAV remains below 1 for an extended period, equity issuance becomes economically unfavorable, capital access tightens, and the relative cost of preferred instruments rises.

BTC vs MSTR

Looking at Bitcoin and MSTR across different time windows highlights an asymmetric behavior. Over the long run, the amplification mechanism fully plays out. Over five years, a $10,000 investment in MSTR shows performance around +1,272%, versus +566% for Bitcoin over the same period.

This outperformance is explained by the progressive amplification of BTC per share. Each dollar raised above the economic value of the underlying Bitcoin increases the amount of BTC controlled per share, producing a multiplier effect on long-term returns.

In the short run, however, the relationship often reverses. Over the last six months, Bitcoin is up around +6.9%, while MSTR is down roughly 35%. This divergence reflects another key element of the model: dilution. Successive common equity issuances, necessary to sustain accumulation and the financing structure, mechanically weigh on performance when mNAV compresses.

MSTR therefore behaves like a two-regime asset. Amplified over the long term when market conditions allow capital to be raised at a meaningful premium, and diluted in the short term when the premium shrinks or the issuance pace exceeds the market's absorption capacity.

This asymmetry explains why MSTR cannot be treated as a fixed-leverage Bitcoin ETF. Its path depends on the cost of capital, market conditions, and the issuance cadence, creating significant dispersion around BTC performance over short horizons, while enabling structural amplification over longer horizons.

Structural effects of a potential S&P 500 inclusion

Since Q3 2025, Strategy meets all eligibility criteria for the S&P 500: sufficient market cap, adequate float, compliant liquidity, and positive cumulative earnings over the last four quarters under the committee's rules. Inclusion remains discretionary, however, and depends on an explicit decision by the index committee.

An S&P 500 addition would mechanically trigger passive flows from index funds and ETFs tracking the index, representing several trillion dollars in assets under management. These flows, independent of investor decisions because they are "automatic", would provide a major demand base for MSTR.

In the context of Strategy's model, such an inclusion would not change the core logic, but it would change the scale. It would broaden the investor base constrained to index allocation, stabilize access to equity markets, and indirectly support the ability to keep mNAV sustainably above 1, the flywheel's core condition.

Standard & Poor's rating

In October 2025, Standard & Poor's reinstated an active rating on Strategy, assigning it a B- rating, classified under non-bank financial institutions. This is one of the first cases where a major rating agency evaluates a company whose balance sheet is largely composed of Bitcoin, effectively bringing the Bitcoin Treasury Company model into the traditional credit universe.

The rating places Strategy in high-yield territory. S&P highlights concentration risk in a single volatile asset, limited operating diversification, and USD liquidity viewed as constrained. The methodology also excludes Bitcoin from "useful" equity in risk-adjusted capital calculations, treating BTC exposure as a volatility factor rather than a solvency anchor.

Still, receiving a rating, even speculative, materially expands the addressable investor universe. Many bond funds and credit vehicles cannot allocate to unrated issuers, but may, under conditions, hold securities classified as high yield. Strategy thus moves from an off-grid issuer to one that is referenced within credit market allocation models.

For Bitcoin, the impact is indirect but still meaningful. By rating Strategy, S&P introduces a Bitcoin-backed balance sheet into credit risk mapping, alongside corporate bonds and sovereign debt. This recognition does not erase the agency's reservations, but it marks an initial step in integrating a Bitcoin-native model into the traditional financial system.

Stakes of the MSCI consultation

In November 2025, MSCI opened a public consultation on the eligibility of companies whose assets substantially depend on crypto-assets. The index provider is considering excluding certain issuers from equity indices when more than 50% of their assets or enterprise value comes from volatile digital assets. Strategy, with more than 75% of its economic value now correlated to Bitcoin, naturally falls within this scope.

MSCI's rationale is not about solvency or default risk, but about equity index coherence. These indices are designed to reflect companies whose value depends on identifiable operating activities, whereas in Strategy's case, the software contribution has become marginal relative to its Bitcoin balance sheet and financing structure.

A potential exclusion would not affect the balance sheet or solvency, but it could weigh on a key pillar of the model: the stability of passive investor demand. By reducing the structural depth of demand, it could increase the cost of capital in the short term and slow the amplification dynamic, without undermining the model's fundamental viability.

Strategy's premium

Since 2024, many companies have adopted a Bitcoin Treasury Company model, but very few manage to sustain a durable premium above the value of their BTC. The reason is structural. Most are limited to passive holding financed by common equity or debt, without any real ability to monetize the balance sheet.

Metaplanet is a partial exception, with intermittent premium driven mainly by a Japan-specific tax advantage. That premium reflects regulatory asymmetry more than a balance sheet transformation model.

By contrast, Strategy supports its premium with tangible economic foundations: a suite of perpetual preferred shares that turns a non-cash-flow asset into institutional yield streams, an attractive ROC tax treatment, a progressive and systemic issuance capacity, and an accounting, regulatory, and disclosure framework fully aligned with SEC standards.

These elements enable the formation of a structural premium as long as mNAV remains above 1. In practice, very few Bitcoin treasuries have the framework required to sustain such a premium over time. Strategy is the exception, Metaplanet a standalone case, while most other players converge toward NAV due to the lack of a differentiated economic model.

Risks tied to Strategy

Liquidation risk

In public debate, the risk of a "liquidation" of Strategy is often framed as a mechanical scenario where a Bitcoin drawdown would trigger forced selling, similar to an over-collateralized DeFi position. That interpretation does not match Strategy's current capital structure.

Since repaying its Silvergate collateralized loan in March 2023, the company has not used any financing directly backed by its bitcoins. There is therefore no automatic liquidation mechanism linked to BTC price.

The real risk is strictly corporate: the ability to meet financial commitments (interest, preferred dividends, convertible debt service) in an environment where access to capital could tighten. This risk needs to be put in context.

At the end of Q3 2025, Strategy held more than 640,000 BTC at an average cost of around $74,000, while convertible debt represented about 11% of the reserve's economic value. The combined annual burden of interest and dividends is below 1% of BTC NAV, a level compatible with meaningfully worse market conditions.

On top of this, the company built a USD cash reserve in late 2025 to absorb temporary shocks in capital market access and secure several quarters of payments. This cushion materially limits the risk that cyclical stress turns into structural stress.

In that context, the notion of "liquidation" as commonly used does not describe a credible scenario. The true issue is the dynamics of the cost of capital, far more than Bitcoin's price path itself.

Risk of selling Bitcoin

Strategy's historical communication is clear: Bitcoin is the company's long-term strategic asset, and management's stated intent is not to sell. Michael Saylor has repeatedly said the model is designed to maximize accumulation, not rotate the portfolio.

Legally and from a regulatory standpoint, reality is more nuanced. In several recent SEC filings, confirmed in late 2025 by CEO Phong Le, Strategy explicitly reserves the right to sell part of its BTC under unfavorable conditions. These conditions include a sustained contraction in capital access, a prolonged mNAV below 1, or BTC trading below average cost.

This is not a base-case outcome, but a protective option to preserve going-concern continuity and creditor interests. The roughly $1.4 billion cash reserve is specifically intended to push this scenario further out.

As long as this reserve covers multiple quarters of interest and dividend payments, the likelihood of a sale triggered by a simple market shock remains low. BTC sales thus appear as a last-resort tool, not an automatic mechanism.

Debt-related risk

Financial leverage is inherently a risk, but Strategy has clarified its trajectory here. The objective is twofold: reduce leverage to zero by 2029 and transition toward a model funded exclusively by permanent capital.

The remaining convertible notes (around $8.2 billion at end-2025) are the only residual leverage source. The company is no longer issuing new debt and plans to let these instruments convert into common shares as contractual conditions allow.

Each conversion mechanically reduces leverage and removes maturity risk, meaning the obligation to repay principal in cash at a fixed date. Over time, Strategy is targeting a structure fully funded by equity and perpetual preferred shares, which fundamentally distinguishes an amplification model from classic leverage.

In other words, by 2029, Strategy will no longer be a leveraged company, but one financed exclusively by permanent capital (equity + preferred shares). This is what separates the "amplification" model from the old "leverage" model.

Today, Strategy operates around 21% amplification, meaning that in its current setup, a 1% move in BTC translates into about 1.21% for MSTR (over the long run, excluding mNAV changes).

The stated goal is to reach 30% amplification, which corresponds to the point where capital inflows from preferred shares combined with the mNAV premium are sufficient to fund net Bitcoin purchases even without price appreciation. This is the permanent regime Strategy is targeting, because it enables structural Bitcoin accumulation regardless of market conditions as long as mNAV stays above 1.

MSCI exclusion risk

This is the risk we have heard the most about in recent weeks, notably because this information (not publicly disclosed by JP Morgan) is said to have triggered the October 10 liquidation wave across crypto.

The risk of exclusion from MSCI indices does not challenge Strategy's solvency or the viability of its business model. It concerns a more mechanical element: access to passive flows driven by equity indices.

An exclusion from MSCI indices would trigger forced selling estimated between $2.5 billion and $2.8 billion for MSCI USA and World alone, and potentially more if other providers adopted similar methodologies.

The timeline still works in Strategy's favor. MSCI's process is slow and consultative, and the largest MSTR holders are also among MSCI's main institutional clients. The final decision, expected in early 2026, remains open. Information published in recent days points toward non-exclusion.

Outlook for 2026

As 2026 begins, the debate around Strategy mostly focuses on its ability to navigate a phase of premium compression in a more difficult market environment. The central question is now: how does Strategy operate when amplification slows, capital access tightens, and Bitcoin volatility persists?

Mid scenario

In this scenario, Bitcoin trades sideways or moderately higher, while mNAV stays close to 1. Strategy is no longer in an aggressive amplification phase, but in a balance sheet management regime.

The priority becomes fully servicing coupons and dividends, preserving USD liquidity, and gradually continuing the conversion of convertible notes. Bitcoin accumulation slows, but the model remains fully operational.

mNAV compression and a more complicated market environment raise the marginal cost of capital, especially for new issuance. This limits amplification (the core of the model), without undermining operating continuity or the deleveraging path toward 2029.

Bear scenario

In this scenario, Bitcoin remains under sustained pressure (it may enter a bear market or keep ranging at lower levels) and mNAV stays below 1 for multiple quarters. Equity issuance becomes economically unfavorable, amplification is paused, and Strategy adopts a defensive stance.

Priorities shift toward suspending dilutive issuance and using the USD cash cushion to ensure interest and dividend payments. The model temporarily stops producing amplification, without breaking down.

The trajectory then relies on the robustness of the existing balance sheet, the low relative burden of financial obligations, and the absence of any automatic liquidation mechanism.

A more extreme scenario combines multiple elements: mNAV persistently below 1, effective exclusion from major equity indices, and Bitcoin staying below the average purchase price. In that case, the liquidity reserve would be gradually used to maintain payment continuity. Only at that point would partial BTC sales become an option, as a last-resort tool rather than an automatic mechanism.

Bull scenario

In this scenario, Bitcoin's rebound is accompanied by a gradual stabilization of mNAV above 1. Strategy then regains the ability to raise capital at a premium under more favorable conditions.

Amplification resumes in a targeted way, primarily through preferred shares, which limits common equity dilution. Progress toward an amplification level closer to 30% becomes achievable again, without requiring an exceptional market environment.

Conclusion

Over just a few years, Strategy has moved from being a software company to a financial structure whose value creation is centered on holding, managing, and monetizing Bitcoin. This transformation was gradual, starting with BTC accumulation, then pushing the legacy software business to the margins, and ultimately establishing a complex and sophisticated model.

The simplistic take, often repeated in the media, is that Strategy is simply buying Bitcoin with traditional leverage. In reality, the model is far more interesting: adopting a perpetual capital structure, segmenting institutional demand through multiple preferred share series, optimizing the tax treatment of cash flows, and building an amplification model that depends on mNAV.

This structure brings Strategy closer to a Bitcoin-linked bond market of sorts, designed to be resilient to BTC price movements over the long term. The strategic horizon is also quite clear: by 2029, Strategy is targeting the full elimination of convertible debt and a structure financed almost entirely by permanent capital.

We outlined several risk scenarios, but the cross-cutting takeaway is that in 2026, Strategy is no longer truly vulnerable to a simple Bitcoin correction. The determining factor becomes the ability to access capital to sustain the model. Amplification can obviously slow, but the model's structure is not called into question for that reason.

This distinction is essential to understand why many of the crisis narratives that surfaced in late 2025 were more about market panic than structural risk analysis. With this deep dive, you should now have a clearer understanding of how Strategy's model works and what risks it carries.